Cyprus company formation continues to attract entrepreneurs, international businesses, investors and corporate groups looking for a recognised European base for their operations. The jurisdiction combines an established corporate framework, EU membership, an English common law-influenced legal system and a competitive tax environment.

However, setting up a company in Cyprus should not be treated as a purely administrative exercise. Incorporation is only the legal starting point, while the commercial success and tax position of the structure will depend on its ownership, governance, business activity, management, substance and ongoing compliance.

At IBCCS TAX, we support local and international clients with company formation in Cyprus, tax structuring, accounting, corporate administration and post-incorporation compliance. This guide explains what business owners should understand before establishing a Cyprus company in 2026.

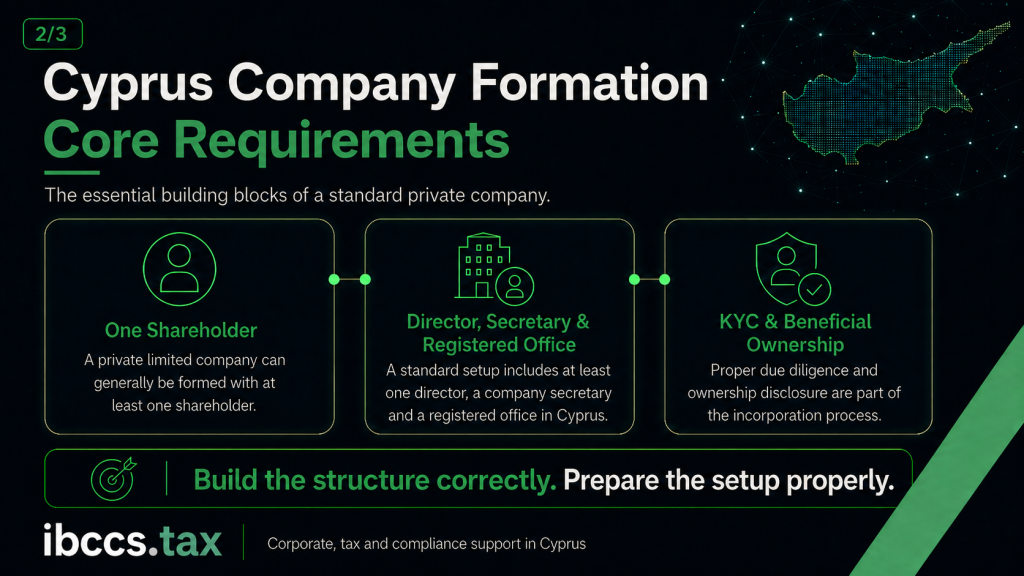

- A Cyprus private limited company can generally be established with one shareholder, one director, a company secretary and a registered office in Cyprus.

- Foreign ownership is permitted, and the incorporation process can often be coordinated remotely, subject to satisfactory KYC and due diligence.

- The standard Cyprus corporate income tax rate is 15% from 1 January 2026 and applies to taxable profits rather than company turnover.

- Incorporation alone does not automatically establish Cyprus tax residency, economic substance or access to tax treaty benefits.

- Company formation should be planned together with governance, VAT, banking, accounting, beneficial ownership reporting and ongoing compliance.

- Cyprus may be particularly suitable for international trading, professional services, technology, IP-led businesses, holding structures and regional operations.

- Working with an integrated tax, legal, accounting and corporate services provider can reduce incorporation delays and prevent structural or compliance issues after registration.

What Does Cyprus Company Formation Involve?

Cyprus company formation is the process of establishing a legal entity under Cyprus law, most commonly a private limited liability company by shares. A standard private company generally requires at least one shareholder, one director, a company secretary, a registered office in Cyprus and properly prepared constitutional documents.

A Cyprus company may be fully foreign-owned and the incorporation process can usually be managed remotely, subject to satisfactory KYC and due diligence. Once the company has been incorporated, further steps may include tax registration, VAT registration where applicable, beneficial ownership reporting, accounting setup, employer registration, banking or payment account onboarding and the implementation of appropriate substance.

The standard corporate income tax rate for Cyprus tax-resident companies is 15% from 1 January 2026. This rate applies to taxable profits rather than revenue, while exemptions and specialised regimes may produce a different effective result depending on the company’s activities and income.

Cyprus Company Formation: Key Information for 2026

| Feature | General position |

| Most common structure | Private limited liability company by shares |

| Foreign ownership | Permitted, subject to due diligence and sector-specific restrictions |

| Minimum shareholders | One |

| Maximum shareholders in a private company | Fifty |

| Minimum directors | One |

| Company secretary | Required |

| Registered office | Required in Cyprus |

| Standard corporate income tax | 15% from 1 January 2026 |

| Annual company levy | Abolished from 2024 onwards |

| VAT registration | Depends on activity, turnover and cross-border transactions |

| Typical incorporation timeframe | Often approximately one to two weeks after completion of KYC and documentation |

| Bank or payment account | Separate onboarding and compliance process |

| Ongoing obligations | Accounting, tax filings, annual return, UBO reporting and other applicable compliance |

These points provide a general overview rather than a complete assessment of a specific structure. The appropriate setup will depend on the intended activity, ownership chain, target markets, personal tax position of the shareholders and the way the company will be managed in practice.

Why Businesses Choose Cyprus for Company Formation

Cyprus is often considered by companies that need an EU-based corporate vehicle for international operations. Its attractiveness is not based on one tax rate or individual benefit, but on the combination of its corporate, legal, tax and business environment.

An Established EU Corporate Jurisdiction

A Cyprus company is established within the legal and regulatory framework of an EU member state. This can provide a recognised corporate platform for businesses operating across European and international markets, although regulated activities and specific cross-border services may require additional authorisations.

The Cyprus legal system is strongly influenced by English common law principles, particularly in areas such as contract law, corporate governance and commercial transactions. This makes the framework familiar to many international investors, lawyers and counterparties.

A Competitive Tax Framework

The standard corporate income tax rate increased from 12.5% to 15% on 1 January 2026. Despite this change, Cyprus continues to provide a competitive corporate tax framework supported by exemptions, deductions, treaty access and specialised regimes.

The effect of the tax system should always be assessed in relation to the company’s actual income and activities. A trading company, holding company, financing company and software business may each have a significantly different tax profile, even when they are all incorporated in Cyprus.

Support for Cross-Border Business

Cyprus has an extensive double tax treaty network and participates in the EU legal and tax framework. Depending on the circumstances, this can support international trading, investment, group ownership, financing and commercial operations.

Treaty or EU directive benefits are not automatic merely because a company has been incorporated in Cyprus. Beneficial ownership, tax residence, substance, anti-abuse provisions and the commercial purpose of the structure must also be considered.

Flexible Ownership and Governance

A Cyprus private limited company can be established with one shareholder and one director. Shareholders and directors may generally be individuals or corporate entities, although the ownership and management structure must remain transparent and pass the applicable compliance checks.

This flexibility allows Cyprus companies to be used by individual founders, joint ventures, family-owned businesses and international corporate groups. The constitutional documents and any shareholders’ agreement should nevertheless be aligned with the intended decision-making process, investment arrangements and future exit plans.

Who May Benefit From Setting Up a Company in Cyprus?

A Cyprus company can support many different business models, but it should have a clear commercial purpose. The jurisdiction may be particularly relevant for businesses that require a credible EU base combined with international operational flexibility.

International Trading and Service Companies

Cyprus may be suitable for consulting firms, professional service providers, marketing companies, international trading businesses and other companies serving clients across multiple jurisdictions. The company’s contracting model, VAT position, transfer pricing exposure and location of management should be reviewed before operations begin.

A Cyprus registration alone does not determine how income will be taxed in every country involved. Cross-border activities may create permanent establishments, local registration requirements or tax exposure outside Cyprus.

Technology, Software and IP-Led Businesses

Technology companies, software developers and businesses generating qualifying intellectual property income may consider the Cyprus IP Box regime. Under the current 15% corporate income tax rate, an 80% exemption on qualifying net IP profits can produce a potential effective rate of approximately 3%, subject to the nexus approach and all qualifying conditions.

The IP Box is not a general reduced rate for every technology company. The intellectual property, development activity, expenditure, ownership and income streams must satisfy the applicable rules, as explained in our guide to the Cyprus IP Box regime.

Holding and Investment Structures

Cyprus is frequently used for holding subsidiaries, receiving qualifying dividends, managing investments and supporting international group structures. Relevant benefits may include exemptions for qualifying dividend income and gains from the disposal of qualifying securities, together with generally limited Cyprus withholding tax on certain outbound payments.

The treatment depends on the source of the income, the underlying assets, the location of subsidiaries and shareholders, and the application of anti-abuse or defensive tax measures. A Cyprus holding company should therefore be structured around genuine commercial objectives rather than a generic template.

Founders Relocating to Cyprus

Some entrepreneurs coordinate setting up a company in Cyprus with their personal relocation. This can create a more consistent relationship between the company’s management, operational presence and the founder’s personal tax position.

Company formation and individual tax residency remain separate matters. Founders considering both should review their corporate structure alongside their change of tax residency to Cyprus and any potential non-domicile position.

Regional Headquarters and International Groups

Cyprus may provide a practical location for companies managing operations across Europe, the Middle East and other international markets. Its professional services sector, multilingual workforce and geographical position can support regional management, administration, finance and coordination functions.

A headquarters structure should demonstrate more than a registered address. The employees, directors, premises, decision-making procedures and operational functions should correspond with the role attributed to the Cyprus entity.

When a Cyprus Company May Not Be the Right Solution

Cyprus is not automatically the best jurisdiction for every business. A structure may be unsuitable where the business has no credible operational or management connection with Cyprus, where the shareholders expect a passive shell with no administration, or where another jurisdiction has a stronger commercial relationship with the activity.

It may also be inappropriate where the business cannot satisfy banking, source-of-funds or regulatory requirements. Selecting Cyprus solely because of a headline tax rate, without reviewing substance and cross-border exposure, can result in a company that is incorporated legally but difficult to operate effectively.

A proper pre-incorporation review should therefore consider:

- where the business will be managed;

- where the owners and key decision-makers are located;

- where employees or contractors will work;

- where customers and suppliers are based;

- which countries will receive or make payments;

- whether the activity is regulated;

- and how profits will ultimately be distributed or reinvested.

The objective should be to establish a structure that supports the underlying business rather than forcing the business into a structure chosen in isolation.

Requirements for a Cyprus Private Limited Company

The private limited liability company by shares is the most common structure used for Cyprus company formation. It creates a separate legal person and limits shareholder liability to the unpaid amount, if any, on the shares held.

A standard private company generally requires the following elements.

Shareholder

At least one shareholder is required and a private company may generally have no more than fifty shareholders. The shareholder may be an individual or a corporate entity, subject to the required due diligence and ownership disclosure.

Where a corporate shareholder is used, the incorporation file will normally need to show the ownership chain up to the ultimate beneficial owners. Group structure charts, corporate certificates and board approvals may also be required.

Director

A private company must have at least one director. Cyprus company law does not impose a universal requirement for every director to be resident in Cyprus, but the composition and location of the board can be highly relevant to tax residency, management and control, substance and operational credibility.

The director should have sufficient authority, information and involvement to perform the role properly. Using a Cyprus-based director should not be treated as a substitute for genuine governance or for the commercial decisions that the company is expected to make.

Company Secretary

A company secretary is required as part of the Cyprus corporate framework. The secretary supports statutory administration, corporate records and filings, although the directors remain responsible for the company’s management and compliance.

For practical reasons, companies commonly appoint a professional secretary familiar with the Cyprus Registrar and local corporate procedures. This can help ensure that changes involving directors, shareholders, registered office or share capital are recorded and filed correctly.

Registered Office in Cyprus

Every Cyprus company must maintain a registered office in Cyprus. This is the company’s formal address for statutory correspondence, notices and corporate records.

A registered office should not be confused with the company’s wider economic substance. Depending on the activity, the business may also require dedicated premises, employees, operational infrastructure or other evidence of genuine presence.

Memorandum and Articles of Association

The Memorandum and Articles of Association establish the company’s constitutional framework. They address matters such as the company’s share capital, governance, director powers and shareholder rights.

Standard documents may be sufficient for a straightforward company, while businesses involving several founders, investors or specialised activities may require more tailored provisions. Important commercial arrangements may also need to be addressed in a separate shareholders’ agreement.

Beneficial Ownership and KYC Information

The ultimate beneficial owners of the company must be identified and disclosed in accordance with the applicable requirements. Professional service providers must also complete KYC and anti-money laundering checks before proceeding with the incorporation and ongoing administration.

The information normally includes identification, residential address, tax residency, professional background, source of funds, source of wealth and a clear explanation of the intended business. More complex structures may require additional corporate records, transaction information or supporting evidence.

Further details on alternative structures can be found in our guide to the types of companies in Cyprus.

Cyprus Corporate Tax in 2026

The standard corporate income tax rate for Cyprus tax-resident companies is 15% from 1 January 2026. The rate applies to taxable profits after permitted deductions and adjustments, rather than to the company’s gross turnover.

The 2026 tax reform introduced several other changes relevant to new and existing companies. These include the extension of tax loss carry-forward from five to seven years, the abolition of deemed dividend distribution for profits generated from 2026 onwards and the abolition of stamp duty for new documents executed from 1 January 2026.

Tax Exemptions and Incentives

Depending on the circumstances, Cyprus companies may also benefit from:

- an exemption for qualifying dividend income;

- an exemption for gains from the disposal of qualifying securities;

- an 80% exemption on qualifying net profits under the IP Box regime;

- notional interest deduction on qualifying new equity;

- group relief subject to the applicable requirements;

- and access to double tax treaties and EU provisions where the relevant conditions are satisfied.

These features should not be considered separately from the company’s commercial activity. The availability of an exemption or deduction will depend on the nature of the income, transaction structure, beneficial ownership, substance and anti-avoidance rules.

A detailed summary of the current changes is available in our Cyprus Tax Reform 2026 guide.

Incorporation and Tax Residency Are Not the Same Question

A company can be legally incorporated in Cyprus without automatically creating the intended tax outcome in every jurisdiction involved. Company tax residency must be considered together with the location of management and control, the company’s decision-making procedures and any relevant double tax treaty.

The place where directors meet, strategic decisions are made, contracts are approved and corporate records are maintained may all be relevant. The role of the shareholders, founders and foreign group management should also be assessed, particularly where important decisions continue to be made outside Cyprus.

This distinction is important because a paper-based corporate structure may not be accepted as representing the company’s real place of management. It can also create uncertainty when applying for tax residency certificates, treaty benefits, bank accounts or regulatory approvals.

Economic Substance for a Cyprus Company

Economic substance should reflect the nature and scale of the company’s actual business. A consulting company, investment holding company and technology business will not necessarily require identical infrastructure, but each should be able to demonstrate that its Cyprus presence is consistent with the functions it claims to perform.

Depending on the business model, substance may include:

- qualified directors based in Cyprus;

- board meetings and strategic decisions taking place in Cyprus;

- physical office space or dedicated premises;

- local employees or appropriately managed service providers;

- accounting and corporate records maintained in Cyprus;

- contracts reviewed and approved through the Cyprus company;

- local banking or payment infrastructure;

- and sufficient operating expenditure relative to the activity.

Substance is not established by adding isolated elements to an otherwise foreign-managed structure. It must be supported by real procedures, documentation and conduct, as discussed in our guide to Cyprus economic substance.

How Does the Cyprus Company Formation Process Work?

The incorporation process is relatively structured, but preparation before filing is often more important than the filing itself. A clear business model, ownership structure and complete KYC file can reduce delays and prevent inconsistencies during later tax or banking onboarding.

At a high level, the process normally includes four stages.

- Structure and Compliance Review

The business activity, shareholders, directors, ownership chain and intended tax position should be reviewed before incorporation. This stage should also identify licensing, VAT, payroll, substance or cross-border considerations that may affect the setup.

Professional service providers will complete due diligence on the relevant shareholders, directors and beneficial owners. Any missing or inconsistent information should be resolved before the incorporation documents are finalised.

- Company Name and Corporate Documents

A proposed company name is submitted for approval. Once the name and structure are confirmed, the Memorandum and Articles of Association and the required incorporation documents are prepared.

The documentation must reflect the agreed shareholders, directors, secretary, registered office and share capital. Additional provisions may be required where the company has several founders, investors or non-standard governance arrangements.

- Filing and Incorporation

The incorporation application is submitted to the Cyprus Registrar of Companies. Once approved, the company receives its registration number, Certificate of Incorporation and standard corporate certificates.

At this point, the company exists as a separate legal entity. It is not necessarily ready to invoice, employ staff, receive regulated income or operate a bank account until the relevant post-incorporation work has been completed.

- Post-Incorporation Setup

The company may then need tax registration, VAT registration, UBO reporting, accounting setup, employer registration, banking onboarding and industry-specific permissions. The exact requirements depend on how and where the company will operate.

A more detailed procedural explanation is available in our article on how to register a company in Cyprus.

How Long Does Cyprus Company Formation Take?

A standard incorporation may often be completed within approximately one to two weeks after the company name, KYC file and incorporation documents are ready. The actual timeframe depends on the complexity of the ownership structure, document certification, name approval and the workload of the relevant authorities.

Company incorporation should not be confused with full operational readiness. Opening a bank or payment account, obtaining VAT registration, onboarding payment providers or securing a regulatory licence may take considerably longer.

Businesses planning a launch date should therefore prepare a wider implementation schedule rather than relying only on the date of incorporation. Contracts, invoicing, banking, bookkeeping and payroll should be coordinated so that the company can operate compliantly from the outset.

How Much Does It Cost to Set Up a Company in Cyprus?

The total cost of setting up a company in Cyprus depends on the structure and the level of support required. Government filing fees represent only one component of the overall formation and onboarding cost.

A complete budget may include:

- name approval and Registrar filing fees;

- preparation of the constitutional documents;

- legal and professional fees;

- registered office and company secretary;

- certified or translated documents;

- director or corporate administration services where required;

- UBO, tax and VAT registrations;

- accounting and bookkeeping setup;

- banking or payment account assistance;

- and substance or office requirements.

Low headline incorporation prices often exclude services that the company will require immediately after registration. A meaningful proposal should clearly distinguish one-off formation costs from annual accounting, tax, corporate administration and substance costs.

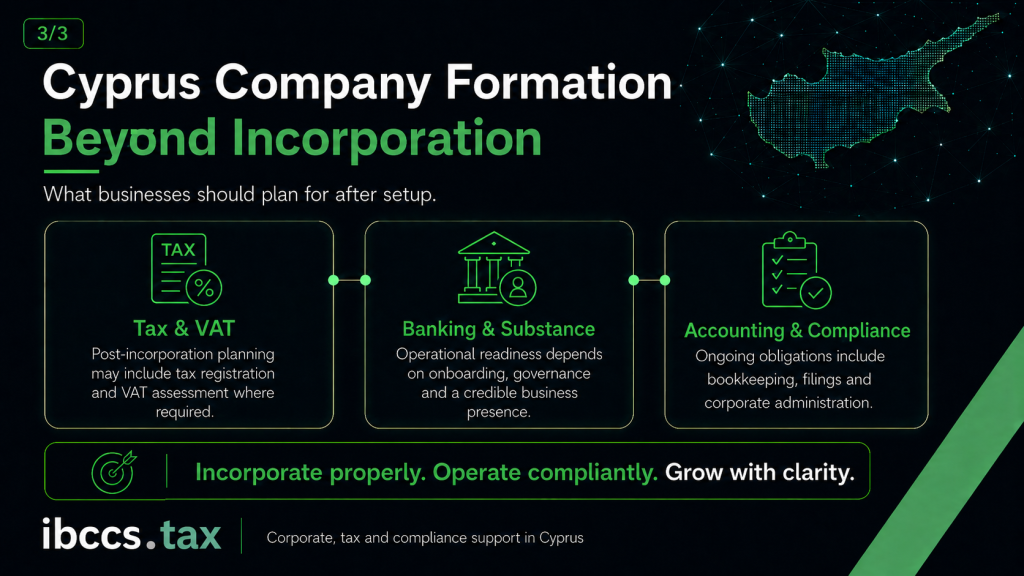

What Happens After the Company Is Incorporated?

Receiving the Certificate of Incorporation is an important milestone, but it does not complete the business setup. A new Cyprus company enters an ongoing compliance framework from the beginning of its operations.

Tax and VAT Registration

The company must be registered appropriately for tax purposes. VAT registration may also be required based on the company’s taxable supplies, expected turnover, intra-EU transactions or other cross-border activities.

The VAT position should be assessed before invoices are issued. Delaying the review can result in incorrect invoices, missed registrations or difficulties recovering input VAT.

Accounting and Financial Reporting

The company must maintain adequate books and records supporting its income, expenditure, assets, liabilities and transactions. The records should be organised from the first transaction rather than reconstructed at the end of the financial year.

Annual financial statements and audit or review requirements may apply depending on the company’s profile and the rules in force. Professional accounting services in Cyprus can also support VAT, payroll, tax returns and management reporting.

Annual Return and Corporate Filings

Cyprus companies must submit an annual return and keep their registered particulars current. Changes to directors, secretary, shareholders, registered office or share capital may require resolutions, updated registers and filings with the Registrar.

The annual company levy of €350 was abolished from 2024 onwards. This did not remove the company’s annual return, financial reporting or other statutory obligations.

Beneficial Ownership Reporting

The company must maintain accurate information regarding its ultimate beneficial owners and complete the required filings and confirmations. Changes in ownership or control should be identified and reported within the relevant timeframe.

The UBO record should remain consistent with the company’s internal registers, corporate documents, tax profile and information supplied to banks or professional service providers.

Payroll and Social Insurance

A company employing staff in Cyprus may need employer and social insurance registration, payroll administration and employment documentation. The timing should be coordinated before employees begin work or receive remuneration.

Cross-border workers, remote employees and directors receiving remuneration may create additional tax, social insurance or permanent establishment considerations. These arrangements should be reviewed rather than treated as ordinary contractor payments.

Banking and Payment Accounts

Opening a bank account is a separate compliance process and is not guaranteed by incorporation. Banks and payment institutions will normally examine the ownership, source of funds, business activity, expected transactions, countries involved and economic connection with Cyprus.

A credible business plan, contracts, customer information and evidence of operations may therefore be as important as the corporate certificates. Our team can assist with the practical process of opening a bank account in Cyprus, subject to each institution’s independent approval.

Common Cyprus Company Formation Mistakes

Many company formation problems arise from decisions made before the company is registered. Correcting an unsuitable ownership, governance or tax structure later can require additional filings, agreements and professional costs.

Common mistakes include:

- selecting Cyprus without reviewing the wider cross-border tax position;

- assuming incorporation automatically establishes substance or tax residency;

- appointing directors who do not genuinely manage the company;

- using generic constitutional documents for a complex shareholder relationship;

- underestimating KYC, banking or source-of-funds requirements;

- issuing invoices before reviewing VAT registration;

- failing to establish accounting procedures from the first transaction;

- ignoring payroll or social insurance obligations;

- and treating the company as a passive registration rather than an operating legal entity.

These issues can usually be reduced through coordinated legal, tax, accounting and corporate planning before the incorporation application is submitted.

Why Work With IBCCS TAX?

Company formation should connect legal registration with the way the business will operate after incorporation. At IBCCS TAX, our Cyprus team combines local implementation with international tax and business experience.

Our support may include:

- pre-incorporation structure and tax review;

- company name approval and incorporation;

- preparation and coordination of corporate documentation;

- KYC and beneficial ownership review;

- registered office and company secretary services;

- tax and VAT registration;

- accounting, bookkeeping and payroll;

- corporate administration and statutory filings;

- banking and payment account coordination;

- substance planning;

- and wider international structuring.

This integrated approach helps ensure that the company is not only incorporated correctly but is also prepared for its tax, accounting and operational responsibilities.

Planning to Form a Company in Cyprus?

Cyprus company formation can provide a strong platform for an international business, but the structure should be designed around the company’s real commercial activity. Ownership, tax residency, management, substance, banking and ongoing compliance should be considered before the incorporation documents are filed.

IBCCS TAX can assist with the full process, from initial structuring and company registration to accounting, tax compliance and ongoing corporate services in Cyprus.

Contact IBCCS TAX to discuss your proposed Cyprus company and the practical steps required to establish it correctly.

Frequently Asked Questions About Cyprus Company Formation

1. Can a foreigner set up a company in Cyprus?

Yes. Foreign individuals and foreign corporate entities may establish and own a Cyprus company, subject to the required identification, beneficial ownership and due diligence procedures.

The shareholder does not normally need to relocate to Cyprus solely to incorporate the company. Personal relocation and tax residency should be assessed separately where they form part of the wider plan.

2. What is the most common type of company in Cyprus?

The private limited liability company by shares is the most common structure. It provides separate legal personality, limited shareholder liability and a flexible framework for local and international business.

Other structures may be appropriate for specialised activities, partnerships, branches or investment arrangements. The legal form should be selected according to the actual commercial objective.

3. What is the Cyprus corporate tax rate in 2026?

The standard corporate income tax rate is 15% from 1 January 2026. It applies to taxable profits of Cyprus tax-resident companies after relevant deductions, exemptions and adjustments.

The effective tax result may differ where the company receives qualifying dividends, disposes of qualifying securities, uses the IP Box regime or qualifies for other deductions.

4. Can a Cyprus company be incorporated remotely?

In many cases, the incorporation can be coordinated without the shareholder travelling to Cyprus. The relevant documents must still be completed, certified and submitted in the required form, while the service provider must complete full KYC and due diligence.

Physical presence may later be useful or necessary for banking, substance, management, employment, licensing or operational reasons. Remote incorporation should not be confused with remote management of the entire business.

5. Is a Cyprus-resident director legally required?

A Cyprus-resident director is not a universal company law requirement for every private company. However, the location and role of the directors can be highly relevant to the company’s tax residency, management and control, substance and banking profile.

The board should be designed around genuine decision-making rather than only formal appointments. The correct approach depends on where the business will actually be managed.

6. How long does it take to register a Cyprus company?

A standard company can often be incorporated within approximately one to two weeks once the name, KYC checks and documents are complete. Complex ownership structures, missing documents or regulated activities may extend the timeframe.

Banking, VAT, licensing and operational onboarding are separate processes. The date on which the company is ready to trade may therefore be later than its legal incorporation date.

7. How much does Cyprus company formation cost?

The total cost depends on the ownership structure, documentation, registered office, secretary, directors, registrations and post-incorporation services required. Government fees are only one element of the overall budget.

Businesses should also plan for ongoing accounting, financial reporting, annual returns, tax compliance and corporate administration. A tailored quotation is more reliable than a package that excludes essential annual services.

8. Does every Cyprus company need VAT registration?

No. VAT registration depends on the company’s taxable activities, turnover, expected transactions and involvement in intra-EU or other cross-border supplies.

The position should be reviewed before the company starts invoicing. Voluntary registration may also be possible or commercially useful in some circumstances.

9. Does incorporation include a Cyprus bank account?

No. Incorporation and bank account opening are separate processes, and every bank or payment institution applies its own risk and compliance assessment.

The company may need to demonstrate its business model, source of funds, counterparties, expected transaction volumes and connection with Cyprus. A Certificate of Incorporation alone is not sufficient to guarantee approval.

10. Does a Cyprus company need economic substance?

The required level of substance depends on the company’s activities, income, governance and international position. A company seeking Cyprus tax residency, treaty benefits or a meaningful operational base should be able to demonstrate genuine management and commercial presence.

Substance may involve directors, premises, employees, expenditure, local records and decision-making in Cyprus. It should reflect the business model rather than a standard checklist.

11. Is a Cyprus company an offshore company?

Cyprus is an EU member state with a regulated and internationally recognised corporate and tax framework. The term “offshore company” is therefore generally inaccurate when referring to a modern Cyprus company.

A Cyprus company is subject to corporate, accounting, tax, beneficial ownership and compliance requirements. It should be established and operated as a transparent legal entity with a genuine commercial purpose.

12. Is Cyprus suitable for an online or software business?

Cyprus may be suitable for online businesses, technology companies and software developers, particularly where the company has international clients and a credible operational connection with Cyprus. The tax, VAT, IP ownership, employee and substance position must nevertheless be reviewed individually.

Software businesses considering the IP Box should confirm that their assets, development expenditure and income satisfy the nexus and qualifying asset requirements. Merely receiving software-related revenue does not automatically produce the reduced effective rate.

Cyprus Company Formation in 2026: Benefits, Requirements, Tax and Compliance

Cyprus company formation continues to attract entrepreneurs, international businesses, investors

Read More

Cyprus Provisional Tax 2026: Deadlines, Rates and Penalties

The first Cyprus provisional tax deadline for 2026 is approaching.

Read More

Cyprus Rent Payment Rules from 1 July 2026: Mandatory Electronic Payments Explained

From 1 July 2026, rent relating to immovable property located

Read More