Cyprus is widely used by international entrepreneurs, investors and corporate groups as a jurisdiction for holding structures. A Cyprus holding company can be an effective vehicle for owning shares in subsidiaries, receiving dividends, centralising group ownership, supporting future exits and organising international investments through a reputable EU jurisdiction.

Cyprus remains a popular jurisdiction for holding company structures because it combines an EU legal environment with several important tax features. These include a 15% corporate income tax rate, generally no Cyprus withholding tax on dividends paid to non-resident shareholders, favourable treatment of qualifying dividend income, an exemption for gains from the disposal of qualifying corporate titles, and access to an extensive double tax treaty network.

These features can be highly relevant for international groups, investment structures and future exit planning. However, they should always be reviewed in the context of the specific ownership chain, shareholder tax residence, substance, beneficial ownership, commercial rationale and applicable anti-abuse rules.

At IBCCS TAX, we support entrepreneurs, private clients and international companies with Cyprus company incorporation, Cyprus tax advisory, accounting, compliance and ongoing corporate administration in Cyprus. This article explains when a Cyprus holding company may be suitable, when it may not be the right option, and what should be considered before setting one up.

What Is a Cyprus Holding Company?

A Cyprus holding company is a Cyprus-registered company established to hold shares or other participations in one or more companies, either in Cyprus or abroad.

Unlike a trading company, which is primarily used to sell goods or services, issue invoices and conduct daily commercial operations, a holding company is typically used for ownership, investment and group structuring purposes.

A Cyprus holding company may be used to:

- hold shares in local or foreign subsidiaries;

- receive dividends from operating companies;

- centralise ownership of an international group;

- support future sale or exit planning;

- hold investments or participations;

- facilitate group reorganisations;

- improve corporate governance and succession planning;

- separate ownership from operational activity.

In practice, a Cyprus holding company can be part of a wider international structure involving operating companies, intellectual property companies, investment vehicles, family holdings or cross-border business groups.

Where intellectual property is involved, the structure should also be reviewed in connection with the Cyprus IP Box Regime, the location of qualifying R&D activity, ownership, licensing arrangements and transfer pricing considerations.

Why Cyprus Is Used for Holding Structures

Cyprus has developed a strong reputation as an international business and holding company jurisdiction. It combines an EU legal and regulatory framework with a competitive corporate tax system, a broad professional services infrastructure and a practical business environment for international groups.

Some of the key reasons why Cyprus is considered for holding structures include:

- EU and Eurozone jurisdiction;

- corporate tax rate of 15%;

- participation exemption for qualifying dividend income;

- generally no withholding tax on dividends paid to non-resident shareholders, subject to applicable exceptions and defensive tax measures;

- exemption for gains from the disposal of qualifying corporate titles, including shares;

- access to an extensive double tax treaty network;

- availability of corporate, accounting and tax advisory services;

- English widely used in business and professional services;

- suitability for regional and international group structures.

For many clients, the value of Cyprus is not based on one tax feature alone. It is the combination of tax efficiency, EU credibility, legal certainty, professional infrastructure and practical access to cross-border advisory support that makes Cyprus attractive.

Cyprus Holding Company: Key Features

| Feature | General Cyprus Position |

|---|---|

| Corporate income tax | 15% from 2026 |

| Outbound dividends | Generally no Cyprus withholding tax on dividends paid to non-resident shareholders, subject to exceptions |

| Dividend income | Qualifying dividend income is generally exempt from Cyprus corporate income tax |

| Share disposals | Gains from the disposal of qualifying corporate titles, including shares, are generally exempt |

| Treaty network | Cyprus has an extensive double tax treaty network |

| EU framework | Cyprus is an EU and Eurozone jurisdiction |

| Common use cases | Group ownership, dividend flows, investment holding, M&A planning, exit planning |

| Key considerations | Substance, beneficial ownership, anti-abuse rules, shareholder tax residence and low-tax jurisdictions |

The table above provides a general overview only. The final tax treatment depends on the exact facts of the structure, including the jurisdictions involved, the nature of the income, the level of substance in Cyprus, the ownership chain and the tax residence of the shareholders.

Key Tax Features of a Cyprus Holding Company

A Cyprus holding company may offer several tax advantages when properly structured. These advantages must always be reviewed in light of the company’s activity, substance, ownership chain, source jurisdictions and applicable anti-abuse rules.

15% Corporate Income Tax Rate

From 2026, the standard corporate income tax rate in Cyprus is 15%. For a trading company, this rate generally applies to taxable business profits.

For a holding company, the effective tax position may be different where the company receives qualifying dividend income or realises gains from the disposal of qualifying titles, as these items may be exempt from Cyprus corporate income tax subject to the relevant conditions.

This is why the tax analysis of a Cyprus holding company should not focus only on the headline corporate tax rate. The type of income, the source jurisdiction, the shareholder structure and the intended use of the company are all important.

Dividend Income Exemption

Dividend income received by a Cyprus company from another company is generally exempt from Cyprus corporate income tax, provided that the relevant conditions are met and anti-abuse rules do not apply.

This is one of the main reasons why Cyprus is often used as a holding company jurisdiction. A Cyprus company may receive dividend income from subsidiaries and use those funds for reinvestment, group financing, distribution to shareholders or further business expansion.

However, the tax treatment should always be reviewed before implementation, especially where the paying company is located in a low-tax jurisdiction, where the dividend is tax-deductible for the paying company, or where the structure involves passive investment income.

No Withholding Tax on Outbound Dividends

In many standard cases, Cyprus does not impose withholding tax on dividends paid by a Cyprus company to non-resident shareholders.

This can be relevant where profits are distributed from a Cyprus holding company to foreign shareholders or reinvested through an international structure.

However, the 0% withholding tax position should not be treated as automatic in every case. The position should be reviewed where the shareholder is located in a low-tax jurisdiction, an EU blacklisted jurisdiction, or where the structure involves associated companies and passive income flows.

The shareholder’s jurisdiction, ownership chain, beneficial ownership position, substance and anti-abuse rules should therefore be reviewed before distributions are made.

Exemption for Gains from Disposal of Qualifying Titles

Cyprus is also attractive for holding structures because gains from the disposal of qualifying corporate titles, including shares, are generally exempt from Cyprus corporate income tax.

This can make a Cyprus holding company useful in exit planning, mergers and acquisitions, group reorganisations and investment structures.

For example, a Cyprus holding company may be relevant where shareholders expect a future sale of a subsidiary, investor exit, group reorganisation or share disposal.

This exemption should still be reviewed carefully. Specific rules may apply where the value of the shares is connected with immovable property situated in Cyprus. For this reason, exit planning should be considered before the structure is implemented, not only at the point of sale.

Double Tax Treaty Network

Cyprus has an extensive double tax treaty network. In a holding company context, this may be relevant when dividends, interest or royalties are paid from foreign subsidiaries to a Cyprus company.

Depending on the jurisdictions involved, double tax treaties may help reduce or manage withholding tax exposure in the source country. For holding structures involving EU subsidiaries, the EU Parent-Subsidiary Directive may also be relevant, subject to the applicable conditions and anti-abuse provisions.

Treaty access should not be assumed automatically. Tax authorities increasingly focus on beneficial ownership, substance, limitation provisions, anti-abuse rules and the domestic law of the paying jurisdiction.

Why These Features Matter in Practice

The main tax features of a Cyprus holding company are relevant because they may affect three important stages of an international structure:

- receiving profits from subsidiaries through dividends;

- holding and reinvesting profits at group level;

- exiting or reorganising through the disposal of shares or participations.

For example, a Cyprus holding company may be used to receive dividends from an operating subsidiary, reinvest those funds into another group company, or hold shares until a future sale. In each case, the structure should be reviewed in advance to confirm the tax treatment in Cyprus, the source jurisdiction and the shareholder’s country of residence.

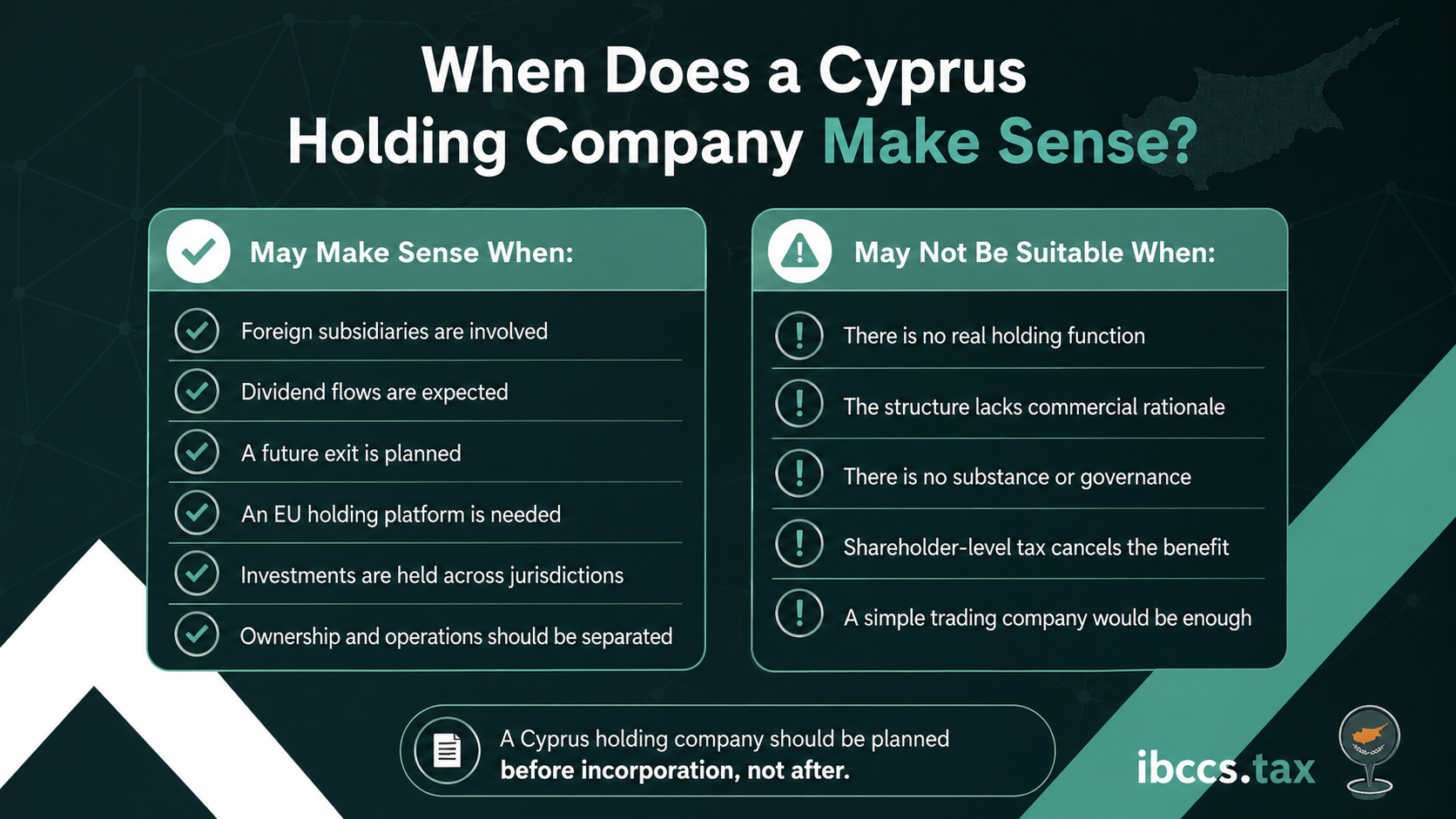

When a Cyprus Holding Company May Make Sense

A Cyprus holding company may be suitable where there is a clear commercial, investment or group structuring purpose.

Below are common scenarios where a Cyprus holding structure may be considered.

- International Group Ownership

A Cyprus holding company may be used as the parent or intermediate holding company for a group with subsidiaries in different jurisdictions.

This can help centralise ownership, simplify group governance and create a clearer structure for dividend flows, reinvestment and reporting.

For example, an international entrepreneur may use a Cyprus company to hold operating companies in different countries, while keeping ownership and strategic decision-making at a central level.

- Dividend Flow Planning

Where a group expects to receive dividends from subsidiaries, Cyprus may be considered as a holding jurisdiction due to the treatment of dividend income and outbound distributions.

For example, a Cyprus holding company may be used to hold shares in an operating subsidiary and receive dividends from that subsidiary. Depending on the jurisdictions involved, the dividend income may be exempt in Cyprus, while Cyprus may also allow onward distribution to non-resident shareholders without Cyprus withholding tax in many standard cases.

This can be particularly relevant for shareholders who want to reinvest profits into new ventures, distribute profits to investors or build a long-term international group structure.

The source jurisdiction, withholding tax rules, treaty access and shareholder-level taxation must be reviewed before implementation.

- Exit and Sale Planning

A Cyprus holding company may be useful where shareholders are planning a future sale of subsidiaries or participations.

As gains from the disposal of qualifying titles are generally exempt from Cyprus corporate income tax, Cyprus can be considered in structures where future share disposals, acquisitions or investor exits are part of the business plan.

For example, a Cyprus holding company may be relevant where the shareholders expect a future sale of a subsidiary. The holding structure should ideally be considered at the planning stage before an investment, acquisition or exit.

This is particularly relevant for founders, investment groups and businesses preparing for regional expansion or future M&A transactions.

- Investment Holding

A Cyprus company may also be used to hold investments, participations or portfolios of companies.

This can provide a structured corporate platform for managing investments, receiving returns and making further acquisitions. The exact treatment depends on the nature of the investments, the source of income and the tax profile of the structure.

For investors holding several participations, a Cyprus company may provide a central EU platform through which investments are owned, monitored and potentially reinvested. This may be useful for corporate groups, family investment structures and entrepreneurs building a portfolio of businesses.

- Separation of Ownership and Operations

In some cases, it may be practical to separate the ownership of shares, intellectual property, investments or strategic assets from the daily trading activity of an operating company.

A holding company can provide this separation and support better risk management, succession planning, group financing or investor participation.

- International Expansion Through Cyprus

Cyprus may also be relevant for businesses expanding into Europe, the Middle East, Eastern Europe or other international markets.

A Cyprus holding company can serve as part of a wider group structure, especially where the business needs an EU base, corporate support, accounting, tax compliance and professional administration.

When a Cyprus Holding Company May Not Be the Right Structure

A Cyprus holding company is not always necessary. In some cases, a simpler structure may be more appropriate. The existence of a 15% corporate tax rate, dividend exemptions, generally no outbound dividend withholding tax and favourable treatment of share disposals does not automatically mean that a Cyprus holding company is the best solution in every case.

A Cyprus holding company may not be the best option where:

- there is only one small local business with no subsidiaries;

- there is no real need for a group structure;

- the company will not hold shares, investments or strategic assets;

- the structure has no commercial purpose beyond tax considerations;

- there is no substance or management in Cyprus;

- the shareholder’s home country tax rules cancel or reduce the expected benefit;

- the group involves low-tax or blacklisted jurisdictions without proper analysis;

- a simple trading company would be more practical;

- the cost and compliance obligations are not justified by the business needs.

The decision should be based on a proper review of the client’s objectives. A holding structure can be very effective when it supports a real business, investment or ownership strategy. It can create unnecessary complexity when used without a clear purpose.

Cyprus Holding Company vs Cyprus Trading Company

A common question is whether a client should set up a Cyprus holding company, a Cyprus trading company, or both.

The answer depends on the role of the company. A holding company is mainly used to own shares, receive dividends, manage investments or centralise ownership. A trading company is mainly used to conduct business activity, issue invoices, employ staff, provide services, sell goods or enter into commercial contracts with clients.

In some cases, one Cyprus company may have both holding and trading functions. In other cases, it may be better to separate the holding activity from the operating activity.

| Feature | Cyprus Holding Company | Cyprus Trading Company |

|---|---|---|

| Main purpose | Ownership and investment | Commercial operations |

| Typical income | Dividends, gains, investment returns | Trading income, service fees, sales revenue |

| Common use | Group structure, subsidiaries, exit planning | Client contracts, invoicing, operations |

| Key considerations | Substance, anti-abuse rules, dividend flows, shareholder taxation | VAT, payroll, permanent establishment, corporate tax, operational risk |

| Best suited for | Groups, investors, founders, international ownership | Active businesses, service providers, e-commerce, consulting, trade |

For many international clients, the right solution may involve both: a holding company for ownership and an operating company for commercial activity. This should be reviewed based on the business model, jurisdictions involved and long-term plans.

How to Register a Holding Company in Cyprus

The registration process for a Cyprus holding company is generally similar to the incorporation of a standard Cyprus private limited liability company. For a broader overview of the incorporation process, you can also read our guide on how to register a company in Cyprus.

The difference is not only in the registration itself, but in how the structure is planned and documented.

The process may include:

- choosing the appropriate company name;

- preparing the corporate structure;

- defining shareholders, directors and secretary;

- preparing the memorandum and articles of association;

- incorporating the company with the Cyprus Registrar of Companies;

- arranging registered office and corporate administration;

- filing beneficial ownership information;

- registering with the Cyprus Tax Department where required;

- assessing VAT or VIES registration if relevant;

- arranging accounting, tax compliance and annual filings;

- reviewing banking or EMI requirements;

- documenting the company’s purpose, governance and substance.

Before incorporation, it is important to review whether the company should be structured as a pure holding company, a mixed holding and trading company, or part of a wider group.

Substance and Management Considerations

International tax planning is increasingly substance-driven. A Cyprus holding company should not exist only on paper if it is expected to benefit from treaty access, tax exemptions or cross-border recognition.

For companies that use Cyprus as part of an international structure, Cyprus company substance requirements should be reviewed together with tax residency, management and control, board composition and the actual role of the company.

Depending on the structure, substance may include:

- Cyprus-based directors involved in decision-making;

- proper board meetings and corporate records;

- a registered office in Cyprus;

- local accounting and tax compliance;

- documentation of commercial rationale;

- substance proportionate to the company’s function;

- evidence of management and control;

- appropriate contracts and intra-group documentation.

The required level of substance depends on the role of the company, the jurisdictions involved and the type of income received. A passive investment holding company may not require the same level of infrastructure as an operating company, but it should still be properly managed and documented.

Important Questions Before Setting Up a Cyprus Holding Company

Before registering a Cyprus holding company, the following questions should be considered:

Where are the subsidiaries located?

The tax treatment of dividends and gains may depend on the jurisdiction of the subsidiary, the local withholding tax rules, the applicable double tax treaty and the tax profile of the paying company.

Where are the shareholders tax resident?

A Cyprus structure must be reviewed not only from the Cyprus perspective, but also from the perspective of the shareholder’s country of tax residence.

Will profits be distributed or reinvested?

A structure designed for reinvestment may require a different approach from a structure intended to distribute profits regularly to individual shareholders.

Is there a planned exit?

If the shareholders plan to sell a subsidiary, bring investors into the group or reorganise ownership, this should be considered before the structure is implemented.

Is there sufficient commercial rationale?

A holding structure should support real business, investment or governance objectives. Structures created only for tax reasons may face scrutiny.

Are any low-tax or blacklisted jurisdictions involved?

From 2026, additional defensive tax measures may apply in relation to certain payments involving associated companies in low-tax or EU blacklisted jurisdictions. This should be checked carefully.

Is the company expected to access treaty benefits?

If treaty benefits are relevant, substance, beneficial ownership and management should be reviewed before relying on treaty protection.

Common Mistakes When Setting Up a Cyprus Holding Company

A Cyprus holding structure can be highly effective when properly planned. However, mistakes at the setup stage can create tax, compliance or practical problems later.

Common mistakes include:

- setting up the company before reviewing the full ownership chain;

- ignoring the tax position of the shareholder’s country of residence;

- assuming that all dividends are automatically tax-free in all cases;

- using Cyprus without sufficient commercial rationale;

- failing to consider substance and management requirements;

- mixing holding and trading activity without proper review;

- not checking withholding tax in the subsidiary jurisdiction;

- ignoring anti-abuse and beneficial ownership rules;

- delaying tax registration, accounting or annual compliance;

- failing to plan for future sale, succession or investor entry.

A holding structure should be designed with the end goal in mind. The best time to review tax, legal and compliance implications is before incorporation, not after the structure has already been implemented.

Cyprus Holding Company for International Entrepreneurs and Investors

A Cyprus holding company may be especially relevant for:

- founders building an international group;

- shareholders planning to acquire or hold foreign subsidiaries;

- businesses expanding into Europe or the Middle East;

- investors holding multiple participations;

- technology companies planning future investment rounds or exits;

- family-owned businesses requiring a clear ownership structure;

- groups looking for an EU-based holding platform;

- entrepreneurs relocating to Cyprus and restructuring their business ownership.

For individuals relocating to Cyprus, the holding structure should also be reviewed together with Cyprus tax residency, Cyprus Non-Dom status, dividend taxation, immigration position and long-term wealth planning.

Corporate and personal tax planning should be aligned. A structure that works well at company level may still require careful review at shareholder level.

Cyprus Holding Company and the 2026 Tax Environment

From 2026, Cyprus applies a corporate income tax rate of 15%. While this represents a change from the previous 12.5% rate, Cyprus continues to offer several important features for international holding structures, including exemptions for certain dividend income and gains from the disposal of qualifying titles.

The 2026 environment also places more emphasis on transparency, substance, anti-abuse rules and defensive measures involving certain low-tax or blacklisted jurisdictions.

For international groups, this means that Cyprus remains attractive, but structures should be reviewed with greater care. The focus should not be only on the headline tax rate. The full structure, income flows, jurisdictions, ownership chain and business purpose should be assessed.

How IBCCS TAX Can Assist

IBCCS TAX provides Cyprus company incorporation, Cyprus tax advisory, accounting, compliance and corporate administration support for clients using Cyprus as part of their business or investment structure.

We can assist with:

- Cyprus company incorporation;

- holding company structuring;

- review of international ownership structures;

- tax advisory for dividend flows and group structures;

- registered office, secretary and corporate administration;

- accounting and annual compliance;

- tax registration and ongoing tax support;

- VAT and VIES registration where applicable;

- beneficial ownership filings;

- support with substance and governance;

- coordination with foreign advisors where cross-border input is required.

A Cyprus holding company can be a powerful tool when it is properly planned and aligned with the client’s commercial objectives. Before setting up the structure, it is important to understand the business model, the shareholders, the subsidiaries, the jurisdictions involved and the long-term plan.

If you are considering a Cyprus holding company, IBCCS TAX can review your situation and assist with the appropriate structure, registration and ongoing compliance.

Frequently Asked Questions: Cyprus Holding Company

1. Is Cyprus a good jurisdiction for a holding company?

Cyprus can be an attractive jurisdiction for holding companies due to its EU status, corporate tax framework, participation exemption for qualifying dividend income, treatment of gains from qualifying titles, double tax treaty network and professional services infrastructure. However, the suitability of Cyprus depends on the ownership chain, source jurisdictions, shareholder tax residency, substance and commercial purpose of the structure.

2. What is a Cyprus holding company used for?

A Cyprus holding company is commonly used to hold shares in subsidiaries, receive dividends, centralise group ownership, manage investments, support future exits, organise international ownership and separate holding activity from trading operations.

3. What is the corporate tax rate for a Cyprus holding company?

The standard corporate income tax rate in Cyprus is 15% from 2026. However, a Cyprus holding company may receive certain types of income, such as qualifying dividends or gains from the disposal of qualifying titles, that may be exempt from Cyprus corporate income tax subject to the relevant conditions and anti-abuse rules.

4. Are dividends received by a Cyprus holding company taxable?

Dividend income received by a Cyprus company is generally exempt from Cyprus corporate income tax, subject to applicable conditions and anti-avoidance provisions. The source of the dividend, the tax treatment in the paying jurisdiction and the nature of the income should be reviewed before relying on the exemption.

5. Does Cyprus have 0% withholding tax on dividends?

In many standard cases, Cyprus does not impose withholding tax on dividends paid to non-resident shareholders. However, this should be reviewed where the shareholder is located in a low-tax jurisdiction, an EU blacklisted jurisdiction or where specific anti-abuse rules may apply.

6. Does Cyprus tax capital gains from share disposals?

Gains from the disposal of qualifying corporate titles, including shares, are generally exempt from Cyprus corporate income tax. Specific rules may apply where the value of the shares is directly or indirectly connected with immovable property situated in Cyprus.

7. How many tax treaties does Cyprus have?

Cyprus has an extensive double tax treaty network. In a holding company structure, this may be relevant for cross-border dividend, interest and royalty flows, depending on the source jurisdiction and applicable treaty conditions.

8. What is the difference between a Cyprus holding company and a trading company?

A holding company is mainly used for ownership, investment and group structuring. A trading company is used for commercial operations, invoicing, contracts, sales, services and active business activity. Depending on the case, a group may require one or both structures.

10. Can a Cyprus company be both a holding and trading company?

Yes, in some cases a Cyprus company may have both holding and trading functions. However, this should be reviewed carefully from a tax, accounting, VAT, substance and risk management perspective. In some structures, it may be better to separate holding and operating activities.

11. Do I need substance for a Cyprus holding company?

Substance is increasingly important in international tax planning. The required level of substance depends on the role of the company, the income received, treaty access, management and control, and the jurisdictions involved. A Cyprus holding company should have appropriate governance and documentation.

12. How long does it take to register a Cyprus holding company?

The timeline depends on the company structure, name approval, documentation, due diligence, shareholder information and any additional registrations required. The process should not focus only on speed; proper structuring before incorporation is often more important than registration alone.

13. Should I set up a Cyprus holding company before acquiring subsidiaries?

In many cases, it is better to review the holding structure before acquiring subsidiaries or making investments. Early planning can help avoid future restructuring, tax inefficiencies or compliance issues.

Moving to Cyprus as a Business Owner in 2026: Tax, Non-Dom & Company Structure

Moving to Cyprus as a business owner can provide access

Read More

Cyprus Tax for Expats in 2026: Foreign Income, Non-Dom & Filing

Cyprus continues to attract entrepreneurs, executives, investors, retirees and internationally

Read More

Cyprus Annual Employer’s Return 2025 and 2026: Form T.D.7 Deadlines and Filing Requirements

The Annual Employer’s Return, Form T.D.7, for the 2025 tax

Read More