International business decisions rarely happen in isolation. A company incorporation, relocation, investment, holding structure, new contract, foreign asset purchase or change in management can all create tax, legal and compliance consequences across more than one jurisdiction. For entrepreneurs and business owners, this is where international tax planning becomes essential.

International tax planning is not only about reducing tax exposure. It is about understanding how your personal position, company structure, income flows, assets, management, substance and reporting obligations interact across different countries. A structure that looks efficient on paper may create risk if tax residency, double tax treaties, permanent establishment, substance, accounting and compliance are not reviewed together.

At IBCCS TAX, we support companies, entrepreneurs, investors and private clients with international tax planning and structuring services across Cyprus, Georgia, the UAE, Uzbekistan and other international markets. This checklist explains what should be reviewed before you expand, relocate or restructure internationally.

- International tax planning helps entrepreneurs understand how personal tax residency, company structure, income flows, assets, management and compliance obligations interact across different jurisdictions.

- Business owners should review their international tax position before incorporating abroad, relocating, restructuring, acquiring foreign assets, expanding into a new market or changing how their company is managed.

- A proper international tax planning review should consider personal and company tax residency, permanent establishment risk, double taxation treaties, withholding tax, substance, transfer pricing, VAT, accounting and reporting obligations.

- Choosing a jurisdiction only because of a low headline tax rate can create risk if management, substance, banking, accounting and compliance are not aligned with the structure.

- IBCCS TAX assists entrepreneurs, investors and companies with international tax planning, corporate structuring and practical implementation across Cyprus, Georgia, the UAE, Uzbekistan and other international markets.

What Is International Tax Planning?

International tax planning is the process of reviewing how business income, personal income, companies, investments, assets and management activities are structured across different jurisdictions. The objective is to create a compliant, commercially practical and tax-efficient structure that reflects the client’s business model, residency position, investment goals and long-term plans.

For entrepreneurs, international tax planning may involve more than one area at the same time. A founder may need to consider personal tax residency, company tax residency, holding company design, dividend flows, intellectual property ownership, VAT, payroll, accounting, reporting, relocation and future exit planning. These elements should not be treated separately, because a decision in one jurisdiction can create consequences in another.

Effective cross-border tax planning should therefore begin before implementation. It is much easier to design the right structure before a company is incorporated, income is moved, assets are transferred or management decisions are made than to correct problems after the structure is already active.

When Do Entrepreneurs Need International Tax Planning?

International tax planning is particularly important when business or personal circumstances involve more than one country. This may include setting up a company abroad, expanding into a new market, relocating personally, changing the place of management, opening a holding company, receiving foreign income, acquiring international assets, restructuring ownership or planning a future sale.

Entrepreneurs often seek advice only when a specific problem appears, such as unexpected withholding tax, questions from banks, uncertainty around tax residency, double taxation, accounting delays or unclear reporting obligations. In practice, these issues are often easier to manage when they are reviewed before the transaction or relocation takes place.

International tax planning may also be relevant when an existing structure no longer reflects the reality of the business. A company may have been incorporated in one jurisdiction, while management, clients, team members, contracts, intellectual property or shareholders are now located elsewhere. When the commercial reality changes, the tax and compliance position should be reviewed as well.

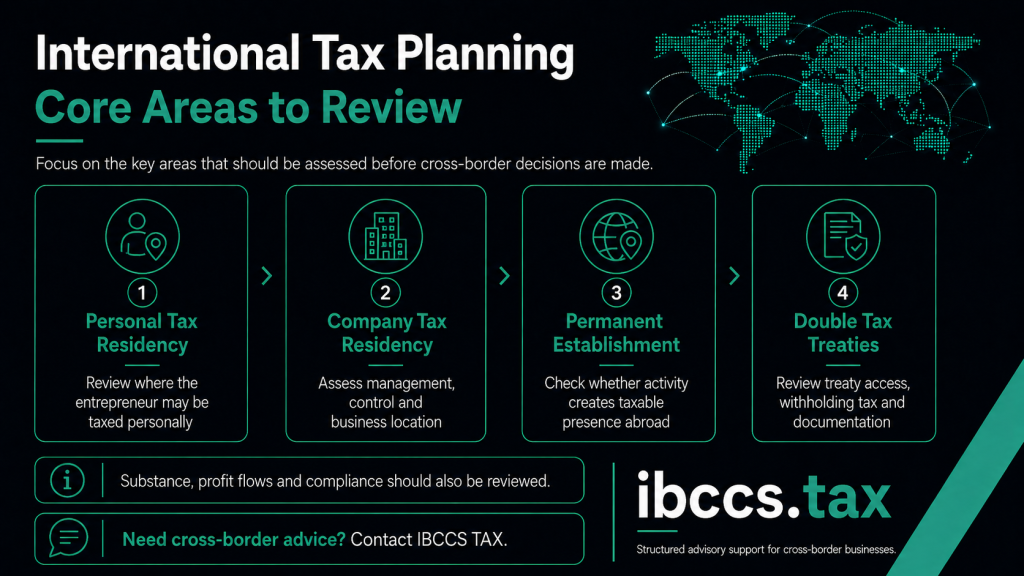

Key Areas to Review in International Tax Planning

| Area to Review | Why It Matters |

| Personal tax residency | Determines where the entrepreneur may be taxed personally and how foreign income, dividends, capital gains or other income may be treated. |

| Company tax residency | Affects where business profits may be taxed and whether management and control are aligned with the intended jurisdiction. |

| Permanent establishment | Can create taxable presence in another country if people, contracts, management or business activity are located there. |

| Double taxation treaties | May reduce double taxation or withholding tax exposure, depending on residency, income type, substance and documentation. |

| Withholding tax | Affects dividends, interest, royalties and other cross-border payments between companies, shareholders or related parties. |

| Substance | Supports the commercial and tax position of the structure and helps demonstrate that the arrangement reflects real business activity. |

| Transfer pricing | Relevant for related-party transactions, including management fees, services, loans, royalties and IP licensing. |

| VAT and reporting | Helps avoid compliance gaps in cross-border trading, digital services, e-commerce or international service provision. |

| Accounting and documentation | Ensures that the structure is properly maintained and supported by records, contracts, invoices, filings and board decisions. |

| Exit and succession planning | Helps prepare for future sale, shareholder changes, asset transfers, family planning or long-term wealth structuring. |

International Tax Planning Checklist for Business Owners

A proper international tax planning review should not focus only on the headline corporate tax rate in one country. The real question is how the full structure works in practice, including residency, management, treaties, substance, profit extraction, reporting and long-term flexibility.

- Personal Tax Residency

For entrepreneurs, personal tax residency is often the starting point. Where you live, how many days you spend in each country, where your family is based, where your economic interests are located and where your business is managed from can all affect your personal tax position.

This is especially important for founders, consultants, remote business owners, investors and internationally mobile individuals. A company structure may be tax-efficient, but if the owner’s personal tax residency is not properly reviewed, income extraction, dividends, capital gains or foreign income may create unexpected consequences.

Clients considering Cyprus as part of their personal tax planning may also need to review tax planning services in Cyprus and, where relevant, Cyprus tax residency and non-domicile considerations. Personal residency should be analysed before relocation, not after the move has already happened.

- Company Tax Residency and Management

A company is not always taxed only where it is incorporated. In many cases, tax authorities look at where the company is effectively managed, where key decisions are made, where directors operate, where board meetings take place and where the real business activity is carried out.

This is a common issue for international entrepreneurs. A company may be registered in one jurisdiction, while the founder, directors, employees or decision-makers operate from another. If this is not reviewed properly, the company may create tax residency or reporting exposure outside the country of incorporation.

Before setting up or restructuring a company, business owners should review whether the proposed jurisdiction is suitable not only from a formation perspective, but also from a management, tax residency, banking and compliance perspective. This is why company setup should be coordinated with company formation and corporate services rather than treated as a purely administrative step.

- Permanent Establishment Risk

Permanent establishment risk can arise when a business has sufficient activity in another country to create taxable presence there. This may happen through a fixed place of business, dependent agents, employees, local operations, management activity or recurring commercial presence.

For international businesses, this risk is often underestimated. A company may invoice from one jurisdiction while sales, negotiations, management, employees or service delivery are taking place in another. If the substance of the business activity is not aligned with the legal structure, tax exposure may arise outside the expected jurisdiction.

Entrepreneurs expanding internationally should review where their people, contracts, clients, management and operations are actually located. This is particularly important for consulting businesses, technology companies, agencies, trading companies, online businesses and groups with teams working across borders.

- Double Taxation Treaty Position

Double taxation treaties can help reduce the risk of the same income being taxed in more than one jurisdiction. They may also affect withholding tax, business profits, dividends, interest, royalties, capital gains and residency conflicts. However, treaties should not be assumed to apply automatically.

A treaty position usually needs to be reviewed together with residency, beneficial ownership, substance, documentation and the type of income involved. In some cases, a structure may appear attractive because a treaty exists, but the practical application may be limited if the company does not have sufficient substance or the income flow is not correctly documented.

International tax planning should therefore include a treaty analysis before key decisions are made. This is especially important for holding companies, cross-border investments, royalty arrangements, financing structures, dividend distributions and groups operating in multiple countries.

- Withholding Tax on Dividends, Interest and Royalties

Withholding tax is one of the most important areas in cross-border tax planning. Even if a company benefits from a favourable corporate tax position, tax may still be withheld when profits are paid out as dividends, interest, royalties or service fees across borders.

Entrepreneurs should review how profits will move through the structure before the structure is implemented. The question is not only where income is earned, but also how it can be distributed, reinvested or transferred without creating unnecessary tax leakage or compliance issues.

This is particularly relevant for international groups, IP structures, financing arrangements, holding companies and businesses with shareholders in different countries. A practical structure should consider both tax efficiency and the ability to move funds in a compliant and commercially workable way.

- Substance and Real Business Activity

Substance has become a central part of international tax planning. Tax authorities, banks and counterparties increasingly expect companies to demonstrate real activity, appropriate management, decision-making capacity, documentation and commercial purpose in the jurisdictions where they operate.

A company with no meaningful presence, no clear management, no proper records and no connection between its structure and its business model may create risk. This can affect tax residency, treaty access, banking, audits, compliance reviews and the credibility of the structure.

Substance does not mean that every company needs a large office or a full local team. The right level of substance depends on the type of business, the jurisdiction, the activities performed and the purpose of the structure. The important point is that the structure should match commercial reality and be supported by proper documentation.

- Corporate Structure and Holding Company Design

A holding company can be useful for international entrepreneurs, investors and business owners who need to manage subsidiaries, investments, intellectual property, dividends, financing, asset protection or future exits. However, a holding structure should be designed with a clear purpose.

Before creating a holding company, it is important to review ownership, tax residency, treaty access, substance, profit flows, reporting obligations, shareholder location, investment plans and exit strategy. A holding company should not be selected only because a jurisdiction is popular or has a favourable tax reputation.

For many clients, the right structure may involve a combination of tax planning, corporate administration, accounting and local implementation. IBCCS TAX assists clients with cross-border structuring and the practical steps required to establish and maintain the structure properly.

- Transfer Pricing and Related-Party Transactions

When companies within the same group trade with each other, transfer pricing may become relevant. This can include management fees, service fees, royalties, financing, cost-sharing arrangements, IP licensing, intercompany loans and other related-party transactions.

The key issue is whether the pricing and documentation reflect commercial reality. Tax authorities may review whether related-party arrangements are consistent with what independent parties would agree in comparable circumstances.

Entrepreneurs should not leave transfer pricing as an afterthought. If a group structure involves more than one entity, related-party transactions should be reviewed before invoices are issued and before profits are allocated between jurisdictions.

- VAT and Indirect Tax Exposure

International tax planning should also consider VAT and indirect tax obligations. A business may be correctly structured from a corporate tax perspective but still face VAT registration, invoicing, reporting or place-of-supply issues.

This is particularly relevant for e-commerce businesses, service providers, SaaS companies, consultants, digital platforms, cross-border traders and businesses supplying clients in multiple jurisdictions. VAT treatment may depend on the type of customer, the place of supply, the nature of the service or goods, and the location of the parties involved.

Accounting and VAT compliance should be reviewed together with the tax structure. IBCCS TAX supports clients with accounting and compliance services to help ensure that the structure is not only designed properly, but also maintained correctly.

- Payroll, Directors and Employee Mobility

People create tax and compliance consequences. Directors, employees, contractors and key decision-makers may affect payroll obligations, social insurance, tax residency, permanent establishment and management and control.

This area is especially important for international entrepreneurs with remote teams, distributed management, relocating founders or employees working from different countries. A company may have been designed around one jurisdiction, while the actual people behind the business are operating elsewhere.

Before relocating a founder, hiring abroad or moving directors between countries, the business should review employment, payroll, tax and immigration consequences. Where relocation is part of the wider plan, it should be coordinated with relocation and immigration services and the broader tax planning strategy.

- Intellectual Property Ownership and Licensing Income

Intellectual property can be one of the most valuable assets in an international business. This may include software, trademarks, platforms, know-how, content, systems, licensing rights or other intangible assets.

Where IP is owned, where it is developed, where it is managed and how it is licensed can all affect the tax and legal position. If the IP structure does not match the real development and management activity, it may create tax, transfer pricing or substance issues.

Entrepreneurs should review IP ownership before transferring assets, signing licensing agreements or setting up multiple entities. This is particularly relevant for technology companies, SaaS businesses, agencies, digital brands, software developers and businesses planning future investment or sale.

- Banking, Accounting and Reporting

A structure is only useful if it can operate properly. Banking, bookkeeping, invoicing, accounting, statutory reporting, tax filings and corporate records are therefore an important part of international tax planning.

Many tax issues arise not because the original idea was wrong, but because the structure was not maintained correctly. Missing records, unclear agreements, late filings, weak documentation, inconsistent invoicing or poor accounting can undermine an otherwise reasonable structure.

Entrepreneurs should review the administrative reality before implementing a structure. This includes which entity will invoice, where records will be kept, who will prepare accounts, what reporting deadlines apply and how management decisions will be documented.

- Exit Planning, Succession and Asset Protection

International tax planning should also consider the future. A structure that works today may not be suitable if the business is sold, shareholders change, assets are transferred, family succession becomes relevant or the founder relocates again.

Exit planning is particularly important for entrepreneurs building companies with long-term value. The tax treatment of capital gains, dividends, share transfers, asset sales and succession should be reviewed before a transaction takes place.

For private clients and families, international tax planning may also involve asset protection, inheritance considerations, ownership structure and long-term wealth planning. These areas should be approached carefully and coordinated with legal, tax and compliance advice.

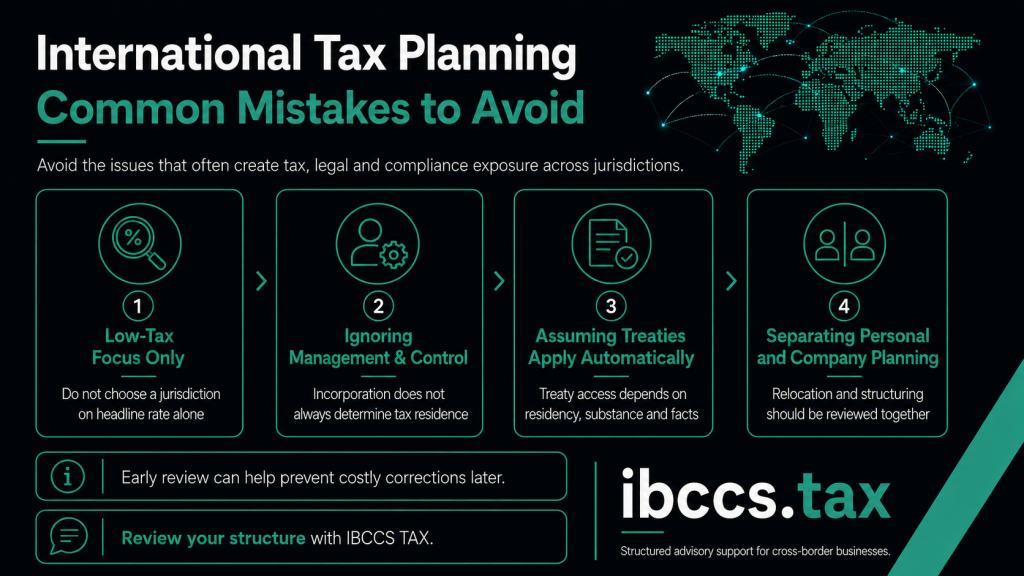

Common International Tax Planning Mistakes

One of the most common mistakes is choosing a jurisdiction only because of a low headline tax rate. Tax efficiency is important, but it should not be separated from residency, substance, reporting, banking, treaty access and commercial purpose. A structure that appears attractive at the beginning may become difficult to operate if these points are ignored.

Another common issue is assuming that incorporation alone determines where a company is taxed. In practice, management, control, directors, business activity and decision-making can all matter. Entrepreneurs who operate internationally should review where the company is actually managed and whether this is consistent with the intended structure.

Many business owners also rely on double taxation treaties without reviewing the practical requirements. A treaty may be relevant, but the correct analysis depends on the type of income, the residency of the parties, beneficial ownership, substance and supporting documentation.

A further mistake is separating personal relocation from company structuring. For founders and owner-managed businesses, the personal tax position of the entrepreneur and the tax position of the company are often closely connected. Relocation, dividends, salaries, director roles and management decisions should therefore be reviewed together.

Not Sure Whether Your Current Structure Is Still Suitable?

If your business, management, clients, assets or personal residency now involve more than one jurisdiction, it may be time to review your international tax position. IBCCS TAX can help assess whether your current structure is still aligned with your commercial activity, tax residency, substance, reporting obligations and long-term objectives.

A review before expansion, relocation or restructuring can help identify potential risks early and support a more practical, compliant and sustainable structure.

International Tax Planning: Why Local Context Matters

International tax planning requires both cross-border perspective and local knowledge. Cyprus, Georgia, the UAE and Uzbekistan may each serve different business, investment or relocation objectives, but the right choice depends on the client’s actual circumstances.

Cyprus may be relevant for entrepreneurs seeking an EU base, holding structures, personal tax planning and international business operations. Georgia may be relevant for regional business activity, entrepreneurs and market entry in the Caucasus. The UAE may be relevant for Gulf business, relocation, trading, holding and international commercial activity. Uzbekistan may be relevant for clients entering or expanding into Central Asia.

The important point is not to select a jurisdiction in isolation. The right structure should reflect the client’s business model, management location, income flows, tax residency, banking needs, compliance obligations and long-term plans.

How IBCCS TAX Can Help with Tax Planning

IBCCS TAX provides international tax planning, structuring, corporate, accounting, legal and relocation support for clients operating across multiple jurisdictions. Through our offices in Cyprus, Georgia, the UAE and Uzbekistan, we help clients assess both the strategic and practical aspects of cross-border decisions.

Our work may include reviewing an existing structure, assessing personal and company tax residency, analysing treaty positions, identifying permanent establishment risk, designing corporate structures, coordinating company formation, supporting accounting and compliance, and assisting with relocation-related tax planning.

For clients planning to expand, relocate or restructure, early advice can help prevent costly corrections later. A proper review before implementation allows the structure to be designed around commercial reality, compliance requirements and long-term objectives.

Planning to Expand, Relocate or Restructure Internationally?

Before making cross-border decisions, it is important to understand how your company, personal residency, management, income flows, assets and compliance obligations fit together. International tax planning helps identify risks, compare options and implement a structure that is practical, compliant and aligned with your goals.

If your business, investments or personal tax position involve more than one jurisdiction, IBCCS TAX can help you review your options and plan the next step with clarity. Contact our international tax advisors to discuss your structure, relocation plans or cross-border business objectives.

FAQ: International Tax Planning

1. What is international tax planning?

International tax planning is the process of reviewing how income, companies, assets, investments and personal tax positions are structured across different jurisdictions. The aim is to create a compliant, commercially practical and tax-efficient structure that reflects the client’s business model, residency position and long-term objectives.

2. Who needs international tax planning?

International tax planning may be relevant for entrepreneurs, investors, companies, shareholders, high-net-worth individuals and families with business, income, assets, management or residency connections in more than one country. It is especially important before expansion, relocation, restructuring, investment or exit planning.

3. Is international tax planning only for large companies?

No. International tax planning can be relevant for SMEs, founders, consultants, digital businesses, holding companies, family businesses and private clients. Many smaller international businesses face cross-border tax issues because their owners, clients, contractors, assets or income flows are located in different jurisdictions.

4. What is the difference between tax planning and tax structuring?

Tax planning is the strategic review of the client’s tax position, objectives, risks and options. Tax structuring is the practical design and implementation of the legal, corporate and operational structure. In cross-border situations, both should be considered together.

5. Can international tax planning help reduce double taxation?

Yes, proper planning can help identify double taxation risks and assess whether treaty relief, foreign tax credits, exemptions or alternative structuring options may be available. The analysis depends on the jurisdictions involved, the type of income, residency, substance and documentation.

6. Why is tax residency important in international tax planning?

Tax residency can determine where an individual or company is subject to tax and reporting obligations. For entrepreneurs, both personal tax residency and company tax residency should be reviewed because the two positions can affect salaries, dividends, management decisions, business profits and long-term planning.

7. When should entrepreneurs seek international tax advice?

Entrepreneurs should seek international tax advice before incorporating a company abroad, relocating, expanding into a new market, moving management, hiring internationally, acquiring foreign assets, transferring IP, restructuring ownership or selling a business. Early planning is usually more effective than correcting issues after implementation.

8. How can IBCCS TAX assist with international tax planning?

IBCCS TAX assists clients with cross-border tax advisory, corporate structuring, double taxation treaty analysis, tax residency considerations, company formation, accounting, compliance and relocation-related tax planning. Our team supports clients through local offices in Cyprus, Georgia, the UAE and Uzbekistan, combined with broader international advisory experience.

How Much Does It Cost to Set Up a Company in Cyprus?

The cost of setting up a company in Cyprus cannot

Read More

Types of Companies in the UAE: Mainland, Free Zone and Legal Structures Explained

The United Arab Emirates offers a wide range of structures

Read More

LLC in Georgia Country in 2026: How to Register a Georgian LLC

Georgia, the country in the Caucasus, has become a practical

Read More