The first Cyprus provisional tax deadline for 2026 is approaching. Cyprus tax-resident companies and self-employed individuals expecting taxable income during the year should review their financial position and arrange the first provisional tax instalment by 31 July 2026.

Provisional tax for the 2026 tax year is payable in two equal instalments. The first instalment must be paid by 31 July 2026, while the second instalment must be paid by 31 December 2026.

The 2026 assessment requires particular attention because the standard Cyprus corporate income tax rate increased from 12.5% to 15% from 1 January 2026. Companies should therefore avoid repeating their 2025 provisional tax payment without reviewing the new rate, current profitability, available tax losses and other adjustments affecting their expected taxable income.

Self-employed individuals should also assess their expected chargeable business income for the full year. Where income, expenditure or profitability changes materially after the first instalment, the provisional tax estimate should be reviewed before the second deadline.

- Cyprus provisional tax for 2026 is payable in two equal instalments.

- The first provisional tax instalment is due by 31 July 2026.

- The second provisional tax instalment is due by 31 December 2026.

- Provisional tax applies to Cyprus tax-resident companies expecting taxable profits and self-employed individuals expecting chargeable business income.

- The standard Cyprus corporate income tax rate is 15% for the 2026 tax year.

- Self-employed individuals are taxed under the applicable personal income tax bands.

- The provisional tax estimate can be revised before the end of the tax year if expected taxable income changes.

- If the provisional taxable income is less than 75% of the final taxable income, an additional 10% tax will apply.

- Late payment can result in interest and monetary penalties.

- The official interest rate applicable to overdue tax in 2026 is 3.5% per annum.

What Is Cyprus Provisional Tax?

Cyprus provisional tax is an advance payment towards the income tax expected to become payable for the current tax year. It allows companies and self-employed individuals to pay their estimated annual income tax liability in two instalments during the year rather than settling the full amount after the final taxable position has been established.

For the 2026 tax year, the estimate should reflect the taxable income expected to arise between 1 January and 31 December 2026. The assessment should be based on the information reasonably available at the time, including current financial results, expected revenue, business expenses, available tax losses and other relevant tax adjustments.

The provisional tax paid during the year is credited against the final income tax liability for 2026. It is not a separate tax charged in addition to the annual income tax liability.

A reasonable estimate should be supported by current accounting records and a realistic forecast of business performance for the remainder of the year. It should not be based solely on turnover, invoices issued, available cash or the amount paid in the previous tax year.

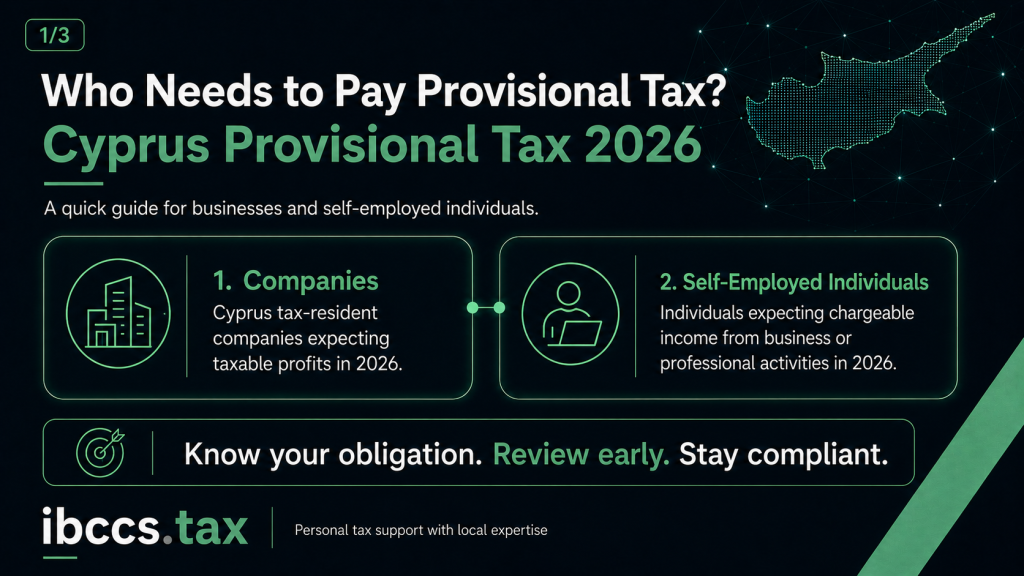

Who Must Pay Provisional Tax in Cyprus in 2026?

Provisional tax is principally relevant to Cyprus tax-resident companies expecting taxable profits and self-employed individuals expecting chargeable income from their business or professional activities.

The obligation depends on whether taxable income is expected during the 2026 tax year. A company or self-employed individual expecting no taxable income may have no provisional tax liability, but this conclusion should be based on a proper review of the expected annual position.

Business performance may change during the year. A company that initially expects a loss may later become profitable after securing new contracts, increasing its margins or completing a significant transaction. A self-employed individual may similarly generate more income than originally anticipated during the second half of the year.

For this reason, the provisional tax position should continue to be monitored even where no payment was initially expected.

Cyprus companies expecting taxable profits

A Cyprus tax-resident company expecting taxable profits during 2026 should assess its provisional corporate income tax liability.

This includes locally operating businesses, international companies managed and controlled from Cyprus, consulting firms, technology companies, professional services businesses, trading companies and other corporate entities carrying on taxable activities.

The amount should be determined by reference to expected taxable profit rather than turnover, gross revenue or available cash. Accounting profit may also differ from taxable profit because specific deductions, exemptions, tax losses and other adjustments may apply.

Accurate and current financial records are therefore essential. Professional accounting services in Cyprus can support companies with bookkeeping, financial reporting, tax compliance and the preparation of their provisional tax position.

Self-employed individuals

Provisional tax also applies to self-employed individuals expecting chargeable income from their business or professional activities during 2026.

This may include consultants, freelancers, independent contractors and professionals carrying on a trade, business or profession in their own name. Their provisional tax liability is determined using the personal income tax rates applicable to their expected chargeable income.

The assessment should consider the income expected from the business for the full tax year, together with allowable business expenditure, deductions and other relevant adjustments. Gross invoices or total business receipts should not be treated as chargeable income without considering the underlying expenses and their tax treatment.

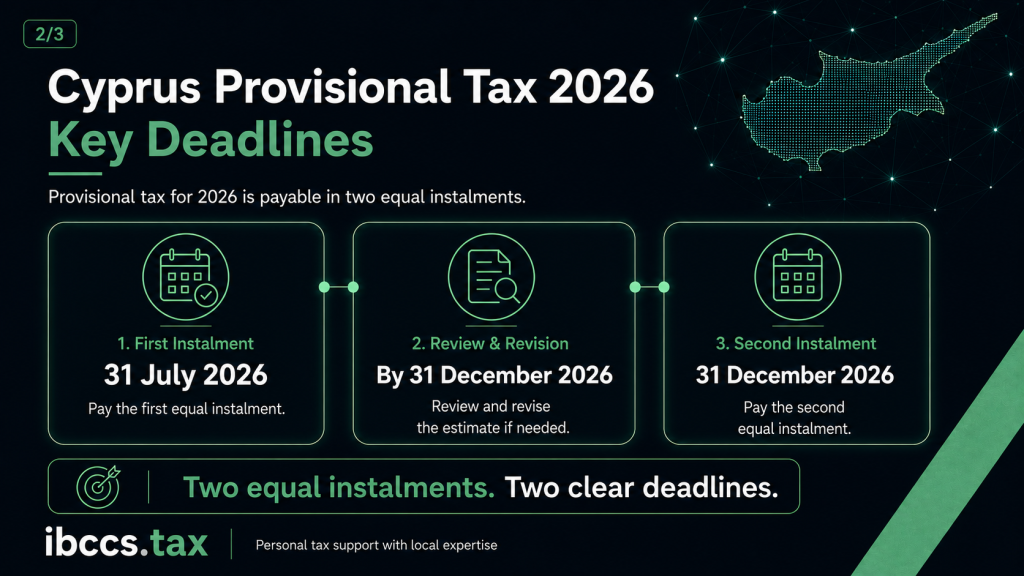

Cyprus Provisional Tax Deadlines for 2026

Cyprus provisional tax for the 2026 tax year must be paid in two equal instalments.

| Provisional tax obligation | Deadline |

| First provisional tax instalment | 31 July 2026 |

| Review and revision of the provisional tax estimate | By 31 December 2026 |

| Second provisional tax instalment | 31 December 2026 |

The first instalment is based on the initial estimate of the annual income tax liability. By the end of July, companies and self-employed individuals should review the financial information available for the first part of the year and prepare a realistic forecast for the remaining months.

Before the second instalment, the original estimate should be compared with the updated expected taxable position for the full year. Where actual performance differs materially from the original forecast, the provisional tax estimate should be revised before 31 December 2026.

The second instalment should not automatically be treated as a repetition of the first payment. It should reflect any valid revision to the expected annual taxable income.

First Provisional Tax Instalment: 31 July 2026

The first Cyprus provisional tax instalment for 2026 must be paid by 31 July 2026.

For companies, the assessment will normally require a review of year-to-date revenue, operating costs, payroll, financing expenses, confirmed contracts and projected business activity for the remainder of the year. Available tax losses and other adjustments affecting taxable profit should also be considered.

Self-employed individuals should review the income already generated through their business or professional activities, expected work for the remainder of the year and expenses that may be deductible in determining their chargeable income.

The objective is not to finalise the annual income tax return in July. It is to establish a reasonable and supportable estimate of the full-year taxable income so that the correct first instalment can be arranged by the deadline.

Second Provisional Tax Instalment: 31 December 2026

The second provisional tax instalment must be paid by 31 December 2026.

Before making the second payment, the business should compare its original estimate with updated financial results and its expected year-end position. This review is important because income, expenditure and profitability can change significantly between July and December.

A company may generate higher taxable profits after securing additional contracts, improving its margins or completing a substantial transaction. Conversely, expected projects may not materialise, revenue may decrease or additional deductible expenditure may arise.

Self-employed individuals may experience similar changes, particularly where their annual income depends on a limited number of clients, projects or assignments. The provisional tax estimate should be revised where the original amount no longer reasonably reflects the expected taxable position for 2026.

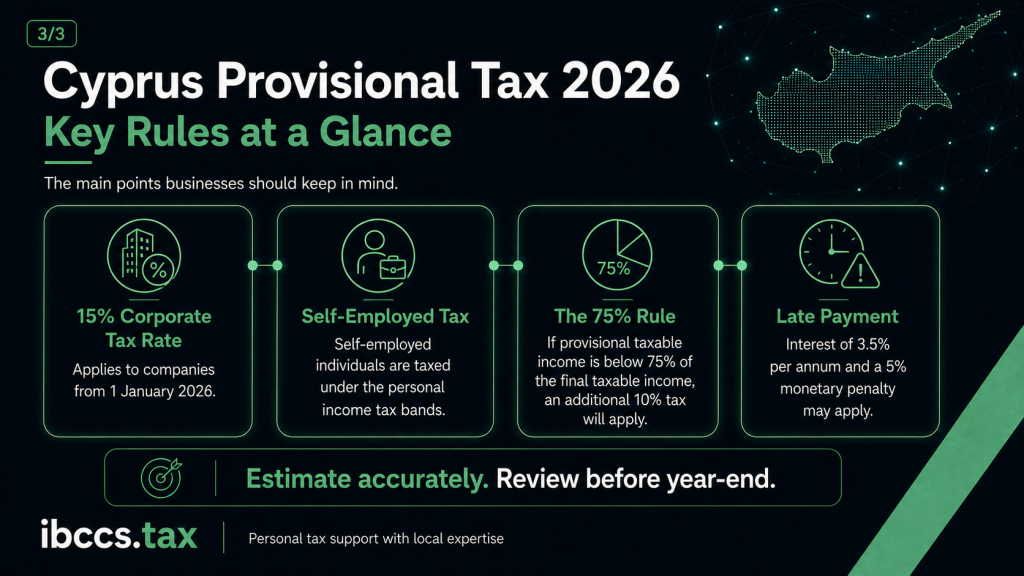

Cyprus Corporate Income Tax Rate for 2026

The standard Cyprus corporate income tax rate increased from 12.5% to 15% from 1 January 2026.

Cyprus companies preparing their provisional tax assessment for 2026 must therefore calculate the expected liability using the 15% corporate income tax rate. Applying the previous 12.5% rate would result in an insufficient provisional tax estimate.

The 15% rate applies to taxable corporate profits rather than gross turnover or accounting revenue. The final taxable result may be affected by available tax losses, allowable deductions, exempt income, non-deductible expenses and other tax adjustments.

Companies should prepare their 2026 provisional tax assessment as a current-year review. Simply repeating the amount paid in 2025, or increasing it without reviewing the underlying taxable profit, may not accurately reflect the amount due.

The wider tax position may also be affected by the changes introduced under the Cyprus Tax Reform 2026. Businesses with cross-border operations, financing arrangements or more complex structures should consider the relevant changes as part of their tax review.

Personal Income Tax Rates for Self-Employed Individuals in 2026

Self-employed individuals are taxed under the personal income tax bands applicable to their chargeable income.

For the 2026 tax year, the personal income tax rates are:

| Annual chargeable income | Tax rate |

| Up to €22,000 | 0% |

| €22,001–€32,000 | 20% |

| €32,001–€42,000 | 25% |

| €42,001–€72,000 | 30% |

| Over €72,000 | 35% |

The rates are progressive, which means that each percentage applies only to the part of chargeable income falling within the relevant band.

The provisional tax estimate should therefore consider the self-employed individual’s expected chargeable income for the full 2026 tax year. Allowable business expenditure, deductions and exemptions may affect the amount subject to tax.

Applying a single tax rate to gross invoices or turnover will not normally provide an accurate result. The calculation should be based on the expected chargeable income after considering the tax treatment of the relevant business income and expenses.

Is Cyprus Provisional Tax Based on Turnover or Taxable Income?

Cyprus provisional tax is based on estimated taxable income, not turnover.

For a company, the starting point is normally the expected accounting result, adjusted in accordance with the applicable tax rules. Certain expenses may not be deductible, while tax losses, exemptions and other allowances may reduce the final taxable profit.

For a self-employed individual, the relevant amount is generally the expected income from the business or professional activity after considering allowable expenses and other adjustments affecting chargeable income.

Turnover may therefore be substantially higher than taxable income. Cash received into a bank account does not necessarily represent the final taxable profit, and accounting profit may not always equal taxable profit.

This is why the provisional tax assessment should be based on reliable accounting information rather than total sales, invoices issued or available cash. Up-to-date bookkeeping services in Cyprus can help businesses maintain the records required to assess their expected profitability and tax obligations.

How Should the 2026 Provisional Tax Estimate Be Prepared?

The provisional tax assessment should reflect the expected taxable position for the full 2026 tax year.

Companies will normally need to review their available management accounts, revenue generated to date, expected income, operating expenses, payroll costs, financing expenses and significant planned transactions. The review should also consider tax losses, exemptions, non-deductible expenses and other differences between accounting and taxable profit.

Self-employed individuals should review their expected business income, anticipated assignments and relevant expenses for the entire year. Changes in the level or nature of the business activity should also be considered where they may affect the final chargeable income.

The estimate should be sufficiently informed to provide a reasonable forecast, but it does not require the final annual income tax return to be completed in advance. The purpose is to determine a supportable expected liability and arrange the two instalments by the applicable deadlines.

Where the tax position involves more complex transactions or adjustments, professional tax planning in Cyprus can help identify the relevant issues and reduce the risk of an inaccurate estimate.

Can the 2026 Provisional Tax Estimate Be Revised?

The provisional tax estimate can be revised where the expected taxable income changes during the year.

The initial estimate is prepared before the final financial result for 2026 is known. A company may secure a major client, complete a profitable transaction or experience stronger growth than expected. A self-employed individual may similarly take on additional projects or generate higher income during the second half of the year.

The opposite can also occur. Revenue may decrease, a significant contract may be cancelled or additional deductible expenses may arise. In such circumstances, the initial estimate may no longer reflect the expected year-end position.

Where the difference is material, the estimate should be revised before 31 December 2026. An upward revision will increase the annual provisional tax liability, while a downward revision may be appropriate where the expected taxable income has genuinely decreased.

Any revision should be supported by the available accounting records and a reasonable forecast of the final result. The ability to revise the estimate should not be used as a basis for declaring an artificially low amount at the first instalment stage.

The Cyprus Provisional Tax 75% Rule

The provisional taxable income declared for 2026 should represent at least 75% of the final taxable income for the year.

If the provisional taxable income is less than 75% of the final taxable income, an additional 10% tax will apply to the difference between the final income tax liability and the provisional tax paid.

This rule makes it important to prepare a realistic estimate and review it again before the second instalment. Paying both instalments by the relevant deadlines does not remove the additional 10% tax where the estimated taxable income is materially below the final taxable income.

The 75% test concerns the accuracy of the annual estimate. It is separate from any interest or monetary penalties resulting from late payment.

Rapidly growing businesses, companies with variable income and self-employed individuals whose earnings depend on a small number of high-value projects should pay particular attention to this rule.

What Happens if Cyprus Provisional Tax Is Paid Late?

Failure to pay a provisional tax instalment by the applicable deadline can result in interest and monetary penalties.

The official interest rate applicable to overdue tax in 2026 is 3.5% per annum. A fixed monetary penalty of 5% of the overdue amount can also apply, with further charges potentially arising where the liability remains unpaid.

Late-payment charges are separate from the additional 10% tax under the 75% rule. A business may therefore face interest and penalties because an instalment was paid late and an additional 10% tax because the provisional taxable income was below the required threshold.

Companies and self-employed individuals should arrange each instalment by the stated deadline and ensure that the liability has been correctly recorded and allocated to the appropriate tax year.

Late Payment and Underestimation Are Different Issues

Late payment and underestimation should be treated as separate compliance risks.

A company or self-employed individual may prepare a reasonable estimate but fail to pay an instalment by the deadline. In that situation, the primary exposure relates to late-payment interest and monetary penalties.

Alternatively, both instalments may be paid on time, but the annual taxable income may have been substantially underestimated. In that case, the additional 10% tax under the 75% rule will apply.

Both issues can arise at the same time where the provisional tax estimate is too low and the instalments are also paid late. Regular accounting reviews and timely payment help reduce both risks.

Why Companies Should Not Reuse Their 2025 Provisional Tax Estimate

The amount paid for 2025 may be useful as a reference point, but it should not be carried forward automatically.

The corporate income tax rate has increased from 12.5% to 15%, which means that a company expecting the same taxable profit may still have a higher provisional tax liability for 2026.

The company’s financial position may also have changed. Revenue, operating margins, payroll, financing costs, available tax losses and significant transactions may differ from the previous tax year.

Cross-border activities, related-party transactions, intellectual property income, restructuring and one-off transactions may also affect the final taxable result.

The 2026 provisional tax assessment should therefore be based on current financial information and the tax rules applicable to 2026 rather than on the amount paid in the previous year.

What Information Should Be Reviewed Before 31 July 2026?

Before the first provisional tax deadline, companies and self-employed individuals should ensure that their bookkeeping records and financial information are sufficiently up to date to support a reasonable estimate.

The review should normally include revenue generated during the first part of the year, confirmed contracts, expected income for the remaining months, operating expenses, payroll or contractor costs, financing expenses and significant transactions.

Available tax losses, capital expenditure, non-deductible expenses and exempt income should also be considered where relevant.

Self-employed individuals should review the income generated through their business or professional activity, expected assignments and allowable business expenses. Missing invoices, incomplete expense records and unreconciled bank accounts should be addressed before the assessment is finalised.

The objective is to establish a reliable expected taxable position and avoid basing the payment on incomplete or outdated information.

Common Cyprus Provisional Tax Mistakes in 2026

Using the previous 12.5% corporate tax rate

The 12.5% corporate income tax rate applied to earlier tax years. The 2026 provisional tax assessment for companies must reflect the new standard rate of 15%.

Repeating the previous year’s payment

The 2025 amount may no longer correspond to the current tax rate, profitability or available tax adjustments. It can provide historical context, but it should not replace a current-year review.

Calculating provisional tax from turnover

Turnover is not the same as taxable income. The provisional tax estimate should be based on expected taxable or chargeable income after considering relevant business expenses and tax adjustments.

Failing to review the estimate before December

The first estimate may become outdated after new contracts, higher revenue, reduced business activity or unexpected expenditure. The position should be reviewed before the second instalment deadline.

Underestimating the final taxable income

If the provisional taxable income is below 75% of the final taxable income, the additional 10% tax will apply. A low initial estimate should therefore be revised where updated financial information indicates that the annual taxable income will be higher.

Leaving the assessment until the deadline

The provisional tax review may require updated accounting records and an analysis of significant transactions. Starting the process too late can increase the risk of an incomplete assessment or missed payment.

Cyprus Provisional Tax 2026 Checklist

Before the first provisional tax deadline, companies and self-employed individuals should confirm that:

- the expected taxable position for 2026 has been reviewed;

- bookkeeping records are sufficiently up to date;

- projected income and expenditure have been considered;

- significant transactions have been identified;

- available tax losses and relevant tax adjustments have been reviewed;

- the 15% corporate income tax rate has been applied where relevant;

- the first equal instalment is arranged by 31 July 2026; and

- a further review is scheduled before the second equal instalment on 31 December 2026.

How IBCCS TAX Can Assist With Cyprus Provisional Tax

A provisional tax assessment should reflect the expected annual taxable income, current financial information and the tax rules applicable to the 2026 tax year.

IBCCS TAX assists Cyprus companies and self-employed individuals with reviewing their expected taxable position, preparing the provisional tax assessment and arranging the relevant tax liability and payments.

Our support can include reviewing management accounts and bookkeeping records, identifying relevant tax adjustments, assessing available tax losses and deductions, preparing the initial estimate and determining whether a revision is required before the second instalment.

Where ongoing support is needed, our accounting services in Cyprus include bookkeeping, financial reporting and tax compliance for local and international businesses. Early preparation gives the business sufficient time to identify missing records, review significant transactions and reduce the risk of late payment or material underestimation.

Review Your Cyprus Provisional Tax Position Before 31 July 2026

The first provisional tax deadline is an important part of the annual Cyprus tax compliance cycle. Companies and self-employed individuals should review their expected taxable position and arrange the first equal instalment by 31 July 2026.

For companies, the 2026 assessment must reflect the increase in the standard corporate income tax rate to 15%. Self-employed individuals should ensure that the estimate reflects their expected chargeable business income and the personal income tax rates applicable to 2026.

The position should then be reviewed before the second equal instalment, which must be paid by 31 December 2026. Where expected taxable income has changed, the provisional tax estimate should be revised to reduce the risk of the additional 10% tax.

IBCCS TAX can assist with reviewing the expected taxable position, preparing the provisional tax assessment, arranging both instalments and determining whether a revision is required before the end of the year. Contact IBCCS TAX to review your Cyprus provisional tax position for 2026.

Frequently Asked Questions About Cyprus Provisional Tax 2026

1. What are the Cyprus provisional tax deadlines for 2026?

Cyprus provisional tax for 2026 must be paid in two equal instalments. The first instalment is due by 31 July 2026, and the second instalment is due by 31 December 2026.

2. Who must pay provisional tax in Cyprus?

Provisional tax applies to Cyprus tax-resident companies expecting taxable profits and self-employed individuals expecting chargeable business income during the tax year.

3. Is provisional tax paid in equal instalments?

Yes. The provisional tax liability for 2026 is paid in two equal instalments due on 31 July and 31 December.

4. What is the Cyprus corporate income tax rate for 2026?

The standard Cyprus corporate income tax rate is 15% from 1 January 2026.

5. Do self-employed individuals pay provisional tax in Cyprus?

Self-employed individuals may be required to pay provisional tax where they expect to generate chargeable income from their business or professional activities during 2026.

6. Is provisional tax based on turnover?

No. Provisional tax is based on estimated taxable or chargeable income, not gross turnover or total invoices.

7. Can the provisional tax estimate be revised?

Yes. The estimate can be revised if the expected taxable income changes during the year. Any necessary revision should be completed before the second instalment deadline on 31 December 2026.

8. What happens if business income increases after July?

Where updated financial information indicates that annual taxable income will be higher than initially estimated, the provisional tax assessment should be revised before the second instalment.

9. What is the 75% rule for Cyprus provisional tax?

The provisional taxable income should be at least 75% of the final taxable income. If it is below this threshold, an additional 10% tax will apply to the difference between the final income tax liability and the provisional tax paid.

10. What happens if provisional tax is paid late?

Late payment can result in interest and a fixed monetary penalty. The official interest rate applicable to overdue tax in 2026 is 3.5% per annum.

11. Is there a penalty for underestimating provisional tax?

Yes. If the provisional taxable income is less than 75% of the final taxable income, an additional 10% tax will apply.

12. Is provisional tax required if a company expects a tax loss?

A company that reasonably expects no taxable income for 2026 may have no provisional tax payment to make. However, the position should be monitored and reviewed if business performance changes during the year.

13. Is provisional tax required if a self-employed individual expects no chargeable income?

A self-employed individual who reasonably expects no chargeable income for 2026 may have no provisional tax payment to make. The expected position should nevertheless be reviewed if the business generates additional income during the year.

14. Should a company use its 2025 provisional tax amount for 2026?

The 2025 amount may be used as background information, but it should not be repeated without review. The 2026 assessment must reflect the new 15% corporate income tax rate and the company’s current expected taxable profit.

15. Should the provisional tax estimate be reviewed again in December?

Yes. The initial estimate should be compared with updated financial results before the second instalment. Where expected taxable income has changed, the estimate should be revised.

Cyprus Tax for Expats in 2026: Foreign Income, Non-Dom & Filing

Cyprus continues to attract entrepreneurs, executives, investors, retirees and internationally

Read More

Cyprus Annual Employer’s Return 2025 and 2026: Form T.D.7 Deadlines and Filing Requirements

The Annual Employer’s Return, Form T.D.7, for the 2025 tax

Read More

International Tax Planning for Entrepreneurs: A Practical Checklist Before You Expand, Relocate or Restructure

International business decisions rarely happen in isolation. A company incorporation,

Read More