The Cyprus Tax Department has announced that the electronic submission system for the Individual Income Tax Return for the 2025 tax year, commonly referred to as Form IR1 or TD1, is now available through TAXISnet.

Employees, pensioners and self-employed individuals who meet the applicable income criteria should review their filing obligations and begin preparing for the submission process. The deadline for submitting the 2025 personal income tax return and paying any resulting tax liability is 31 October 2026.

A late submission may result in an administrative penalty of €150. Taxpayers are therefore encouraged not to leave the preparation of their return until the final weeks before the deadline.

Visit our dedicated Income Tax Return for Individuals service page to learn more about the scope of our support.

- The Cyprus IR1 submission system for the 2025 tax year is now open.

- The filing and payment deadline is 31 October 2026.

- A late submission may result in a €150 administrative penalty.

- Employees, pensioners and self-employed individuals whose gross income exceeded €19,500 should review whether they are required to file.

- Additional care may be needed where an individual has foreign income, several income sources, company involvement or cross-border tax matters.

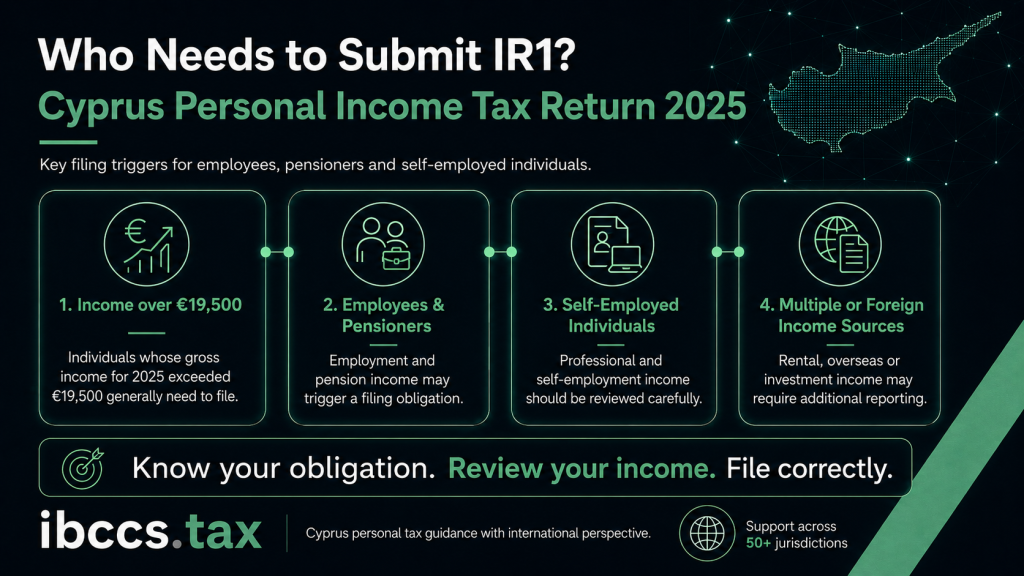

Who Must Submit a Cyprus Personal Income Tax Return for 2025?

Employees, pensioners and self-employed individuals whose total gross income for the 2025 tax year exceeded €19,500 are generally required to submit an individual income tax return.

Gross income may include income from employment, self-employment, pensions, property, investments or sources outside Cyprus. The precise filing and reporting position will depend on the individual’s circumstances.

Particular attention may be required where an individual has:

- more than one source of income;

- income arising outside Cyprus;

- self-employment or consultancy activity;

- rental or investment income;

- an interest in or remuneration from a company;

- cross-border tax or residence considerations.

Tax residence and tax return filing obligations should also be considered separately. Being registered as a Cyprus tax resident does not automatically determine the treatment of every source of income, particularly where another country may also have taxing rights.

Professional advice may therefore be appropriate where an individual’s position involves more than straightforward Cyprus employment income.

Cyprus IR1 Submission Deadline for the 2025 Tax Year

The deadline for the electronic submission of the 2025 personal income tax return and the payment of any resulting tax liability is:

31 October 2026

Returns must be submitted electronically through the TAXISnet platform. Taxpayers should ensure that their return is prepared accurately, submitted within the applicable deadline and supported by information reflecting their complete income position. The amount of tax payable, if any, will depend on the individual’s income, deductions, tax residence, personal circumstances and other relevant factors.

What Is the Penalty for Filing the IR1 Late?

A late submission of the 2025 individual income tax return may result in an administrative penalty of €150.

Additional interest, surcharges or other charges may arise where a tax liability remains unpaid after the applicable deadline. Submitting the return on time is therefore only one part of the compliance process. Individuals should also ensure that their income position has been reviewed correctly and that the return does not contain material omissions or inconsistencies.

An inaccurate or incomplete return may create compliance issues even where it is submitted before 31 October 2026.

When Can an IR1 Return Become More Complex?

The complexity of a Cyprus personal income tax return depends on the individual’s income sources, tax residence and wider personal or business circumstances.

Additional consideration may be required where the taxpayer has:

- foreign-source income;

- income from several employers or business activities;

- self-employment income;

- rental, dividend or interest income;

- directorships or shareholdings;

- income connected with a Cyprus or overseas company;

- potential foreign tax relief;

- Cyprus tax residence or non-domicile considerations.

In such cases, the correct treatment may depend on Cyprus tax legislation, the nature and source of the income and any applicable double tax treaty. Seeking professional support can help ensure that the return reflects the individual’s actual tax position and that relevant issues are identified before submission.

Reporting Foreign Income in a Cyprus Personal Tax Return

Individuals who are Cyprus tax residents may need to consider income arising both in Cyprus and abroad.

Foreign-source income may include employment, professional, pension, property, investment or other income generated outside Cyprus. The existence of foreign income does not necessarily mean that the same income will be taxed twice. Cyprus has an extensive network of double tax treaties, and relief may be available where the relevant conditions are satisfied.

However, foreign income should not be disregarded simply because tax has already been paid in another jurisdiction. Its treatment will depend on the type of income, the taxpayer’s residence position, the applicable Cyprus rules and any relevant treaty provisions.

IBCCS TAX provides personal income tax return services in Cyprus for individuals with local and international income, including support with IR1 preparation, foreign income reporting and cross-border tax matters.

Why Accurate IR1 Filing Is Important

The IR1 return forms part of an individual’s official tax record in Cyprus.

An accurately prepared and submitted tax return may be relevant when an individual needs to:

- demonstrate Cyprus tax compliance;

- support an application for a Cyprus Tax Residency Certificate;

- respond to a bank or compliance request;

- document income for financing or investment purposes;

- support an immigration or relocation process;

- maintain a clear and consistent tax history.

Discrepancies between a tax return, employer information, company records, banking information and declarations made in another jurisdiction can lead to further questions or requests for clarification.

It is therefore important that the return reflects the taxpayer’s broader financial and tax position rather than relying only on information that may already appear in an electronic system.

Common Issues When Completing the Cyprus IR1

Although certain information may already be available electronically, taxpayers remain responsible for the accuracy and completeness of their return.

Common issues may include:

- omitting a source of income;

- incorrectly treating foreign income;

- applying deductions or reliefs incorrectly;

- failing to consider relevant tax residence matters;

- inconsistencies with payroll or company records;

- submitting or paying after the applicable deadline.

More complex situations can arise for company directors, shareholders, consultants, remote workers, individuals with overseas property and internationally mobile professionals. In these cases, the preparation of the return should be considered together with the individual’s broader tax and business position.

How IBCCS TAX Can Assist With Your 2025 Personal Income Tax Return

IBCCS TAX supports employees, executives, company directors, pensioners, self-employed professionals, entrepreneurs and internationally mobile individuals with their Cyprus personal income tax obligations. Our assistance may include:

- reviewing whether an IR1 filing obligation applies;

- preparing and electronically submitting the 2025 personal income tax return;

- reviewing Cyprus and foreign-source income;

- calculating relevant tax and General Healthcare System liabilities;

- considering available deductions, allowances and tax reliefs;

- reviewing foreign tax and double tax treaty considerations;

- coordinating personal income with payroll and company accounting records;

- assisting with Cyprus tax residence and non-domicile matters;

- providing personal and international tax advisory.

Where a client is also a shareholder, director or employee of a Cyprus company, our team can coordinate the personal tax return with the company’s accounting, payroll and compliance records. This coordinated approach can help reduce inconsistencies and ensure that the personal tax return reflects the taxpayer’s wider financial and business position.

Learn more about our dedicated Income Tax Return for Individuals service in Cyprus.

Need Assistance With Your Cyprus IR1 for 2025?

The 2025 Cyprus personal income tax return must be submitted by 31 October 2026. A late filing may result in a €150 administrative penalty, while delayed payment may lead to additional interest and charges.

Professional support may be particularly important if you have foreign income, several sources of income, self-employment activity, rental or investment income, company involvement or cross-border tax matters. IBCCS TAX can assist with reviewing your filing obligation, preparing the IR1 return, calculating the relevant liabilities and completing the electronic submission.

Frequently Asked Questions About the Cyprus IR1 for 2025

1. What is the deadline for submitting the Cyprus IR1 for 2025?

The deadline for submitting the individual income tax return for the 2025 tax year is 31 October 2026. Any resulting tax liability should also be paid by the applicable deadline.

2. Who must submit a personal income tax return in Cyprus for 2025?

Employees, pensioners and self-employed individuals whose total gross income for 2025 exceeded €19,500 are generally required to submit an individual income tax return. The precise obligation may depend on the individual’s income sources, tax residence and personal circumstances.

3. What is the penalty for submitting the IR1 late?

A late submission of the 2025 individual income tax return may result in an administrative penalty of €150. Further interest or charges may apply where tax is also paid late.

4. How is the Cyprus IR1 submitted?

The return is submitted electronically through the TAXISnet system. Individuals remain responsible for ensuring that the information included in the return is complete and accurate.

5. Do I need to report foreign income in my Cyprus tax return?

Cyprus tax residents may be required to consider income received from both Cyprus and foreign sources. The correct tax treatment depends on the type of income, the taxpayer’s residence position, Cyprus legislation and any applicable double tax treaty.

6. Do I need to submit an IR1 if my income is below €19,500?

An individual whose total gross income does not exceed €19,500 may not be required to submit an IR1 under the general income threshold. However, other circumstances, registrations or specific requirements may still need to be considered.

7. Can foreign tax paid be credited against Cyprus tax?

Foreign tax relief may be available where the same income has been taxed in another country. The availability and calculation of the relief depend on the circumstances, supporting information, Cyprus legislation and any applicable double tax treaty.

8. Are dividends and interest relevant to the IR1?

Dividends and interest may need to be considered when preparing the return, even where they are not subject to Cyprus income tax. Their treatment may also depend on the individual’s tax residence, domicile status and General Healthcare System obligations.

9. Can IBCCS TAX prepare and submit my personal income tax return?

Yes. IBCCS TAX can review your filing obligation, prepare the return, calculate the relevant liabilities and assist with electronic submission. Our team can also advise on foreign income, Cyprus tax residence, non-domicile status and related international tax matters.

Prepare and Submit Your 2025 IR1 With Professional Support

Visit our dedicated Income Tax Return for Individuals service page to learn more about the scope of our support.

To discuss your personal circumstances and begin preparing your 2025 Cyprus income tax return, contact IBCCS TAX. Our Cyprus team provides coordinated support covering personal income tax returns, Cyprus tax residence, foreign income reporting, accounting and international tax matters.

International Tax Planning for Entrepreneurs: A Practical Checklist Before You Expand, Relocate or Restructure

International business decisions rarely happen in isolation. A company incorporation,

Read More

Cyprus Company Formation in 2026: Benefits, Requirements, Tax and Compliance

Cyprus company formation continues to attract entrepreneurs, international businesses, investors

Read More

Cyprus Provisional Tax 2026: Deadlines, Rates and Penalties

The first Cyprus provisional tax deadline for 2026 is approaching.

Read MoreThis publication is intended for general informational purposes only and does not constitute tax, legal or financial advice. The application of Cyprus tax rules depends on the facts and circumstances of each individual case.