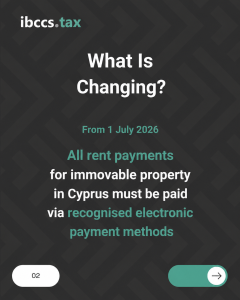

From 1 July 2026, rent relating to immovable property located in Cyprus must be paid exclusively through an accepted electronic payment method.

The requirement was introduced under Article 48A of the Assessment and Collection of Taxes Law, Law No. 4/1978, as part of the broader Cyprus tax reform 2026. It affects landlords, tenants, companies, self-employed persons and other individuals or legal entities involved in rental arrangements concerning property situated in Cyprus.

Earlier commentary on the reform frequently referred to a €500 monthly threshold. However, the latest official announcement issued by the Cyprus Tax Department in June 2026 confirms that the requirement applies regardless of the amount of rent and regardless of the type or use of the immovable property. Accordingly, landlords and tenants should not rely on the previously reported €500 threshold. Based on the latest official position, all Cyprus rent payments must be made electronically from 1 July 2026.

- Mandatory electronic rent payments apply from 1 July 2026.

- The rules cover rent relating to immovable property situated in Cyprus.

- The obligation applies to both individuals and legal entities.

- It applies regardless of the amount of rent.

- It applies to residential, commercial and other property uses.

- Permitted methods include bank transfers, debit or credit cards and other recognised electronic payment methods.

- Landlords may not accept rent through a non-compliant payment method.

- Rent paid in breach of Article 48A may not qualify as a tax-deductible expense.

- Lease terms, payment procedures, bookkeeping records and supporting documentation should be reviewed before the effective date.

What Is Changing for Cyprus Rent Payments?

Article 48A introduces a mandatory payment framework for rent concerning immovable property located in the Republic of Cyprus.

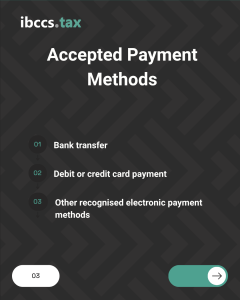

From 1 July 2026, rent must be paid exclusively through:

- bank transfer;

- debit or credit card payment; or

- another recognised electronic payment method.

The obligation is not limited to the person making the payment. A landlord or any other recipient of rental income relating to immovable property in Cyprus may not accept rent through another method. In practice, this means that traditional cash rental arrangements should be discontinued and replaced with a payment process that creates a clear, verifiable and retainable transaction record.

For companies and self-employed persons, the change should also be integrated into their wider accounting services in Cyprus, internal controls and tax compliance procedures.

Cyprus Rent Payment: Does the €500 Rent Threshold Still Apply?

Earlier summaries of the Cyprus tax reform often stated that only rent payments of €500 or more per month would need to be paid electronically. This interpretation appeared in a number of professional, legal, real estate and tax-related publications issued before the Cyprus Tax Department’s June 2026 clarification. Some of those publications described the reform as applying only to monthly rent exceeding €500.

However, the official announcement published by the Cyprus Tax Department in June 2026 does not retain this threshold. The Department’s current position is that the electronic payment obligation applies:

- regardless of the amount of rent; and

- regardless of the type or use of the immovable property.

Therefore, based on the latest available official guidance, the €500 threshold should no longer be treated as applicable. Landlords, tenants and businesses should arrange for all rent relating to immovable property in Cyprus to be paid through an accepted electronic method from 1 July 2026.

Why Earlier Publications Referred to €500

The discrepancy appears to arise from early market summaries and preliminary commentary on the tax reform. The Cyprus Tax Department’s June 2026 announcement clarified the practical scope of the requirement shortly before the rules were due to enter into force. Its wording is broader and expressly applies to rent regardless of value or property use. For compliance purposes, the latest official position should take precedence over earlier summaries and secondary commentary. Businesses that prepared their procedures on the basis of the previously reported €500 threshold should now update their payment instructions, internal policies and accounting controls.

Which Rental Arrangements Are Covered?

The obligation concerns rent relating to immovable property located in Cyprus.

It may therefore apply to rental payments for:

- residential houses and apartments;

- offices and serviced premises;

- retail shops and commercial units;

- warehouses and storage facilities;

- industrial premises;

- professional offices and clinics;

- employee accommodation;

- short- or long-term business premises; and

- other rented immovable property situated in Cyprus.

The official position applies irrespective of the property’s use. The requirement should therefore not be treated solely as a commercial property rule or solely as a residential tenancy rule. The electronic payment requirement may also be relevant where a Cyprus company rents property from a director, shareholder, connected party or another group entity.

Are Cash Rent Payments Permitted after 1 July 2026?

Cash is not included among the payment methods permitted under Article 48A. From 1 July 2026, rent should be paid through a bank transfer, card payment or another recognised electronic payment method. A landlord should likewise not accept rent in cash or through another method that does not fall within the prescribed framework. A handwritten receipt or acknowledgement of payment does not transform a cash payment into an electronic payment. Although a receipt may remain useful as supporting evidence, it does not replace the requirement to use a compliant electronic payment method.

Landlords who currently collect rent in cash and tenants who currently pay in cash should agree on an alternative payment process before the effective date.

Cyprus Rent Payment Rules: Accepted Payment Methods in Cyprus

Bank Transfer

A bank transfer will generally provide the clearest and most straightforward payment trail. The payment reference should ideally identify:

- the tenant;

- the property;

- the rental period; and

- the purpose of the payment.

Business tenants should normally make the payment from the relevant company or business account rather than through an unrelated personal account.

Debit or Credit Card

Rent may also be paid by debit or credit card where the landlord, property manager or authorised recipient has an appropriate card payment facility. The parties should retain the transaction confirmation and ensure that the payment can be matched to the relevant lease, property and rental period.

Other Recognised Electronic Payment Methods

Article 48A also allows the use of other recognised electronic means of payment. Where a digital payment platform or electronic wallet is used, the parties should ensure that the transaction record clearly shows:

- the payer;

- the recipient;

- the date;

- the amount;

- the payment status; and

- the connection with the rental obligation.

Where there is uncertainty over whether a particular platform qualifies as a recognised electronic payment method, professional clarification should be obtained before relying on it.

Cyprus Rent Payment Rules: Why It Matter for Tax Deductibility

The new framework is not merely an administrative rule governing how rent is transferred. Cyprus tax provisions also connect compliance with Article 48A to the deductibility of rental expenditure. Rent payments made contrary to the prescribed payment requirements may not qualify as tax-deductible.

This is particularly relevant to:

- Cyprus companies renting business premises;

- self-employed persons claiming rental expenses;

- employers renting accommodation for personnel;

- businesses leasing offices, warehouses or retail locations; and

- other taxpayers seeking to deduct rent against taxable income.

A business may have a valid lease and may have genuinely incurred the rental cost. However, if the payment method does not comply with Article 48A, the expense may be disallowed when calculating taxable profit. For example, a company may record rent as an expense in its accounting system. If the payment was made through a non-compliant method, the amount may need to be added back when the company’s taxable profit is calculated.

Businesses should therefore treat the payment method as part of the tax review process rather than merely as a private arrangement between the landlord and tenant. The rules should also be considered together with the wider tax treatment of rental income in Cyprus, which may involve different obligations depending on the status of the landlord, the type of income and the applicable tax regime.

What Landlords Should Do before 1 July 2026

Landlords should review how rent is currently collected and ensure that a compliant electronic payment method is available. Recommended actions include:

- Provide tenants with accurate bank account or electronic payment details.

- Inform tenants in writing that rent must be paid electronically.

- Stop accepting cash rent payments from the effective date.

- Review lease clauses relating to payment methods.

- Retain bank statements and electronic transaction records.

- Match each incoming payment to the relevant tenant, property and rental period.

- Review payments collected through property managers or agents.

- Ensure that rental income is properly reflected in accounting and tax records.

Landlords with multiple properties may benefit from introducing a standard payment-reference format to simplify the reconciliation of incoming payments.They should also avoid accepting rent into accounts belonging to unrelated persons where this could obscure the identity of the legal recipient or create inconsistencies with the lease documentation.

What Tenants Should Do before 1 July 2026

Tenants should confirm the correct electronic payment details with the landlord or authorised property manager. They should also ensure that every payment creates evidence of:

- the amount paid;

- the date of payment;

- the identity of the recipient;

- the relevant property;

- the applicable rental period; and

- the successful completion of the transaction.

Where a landlord continues to request cash payment after 1 July 2026, the tenant should ask for a compliant electronic alternative and retain the relevant correspondence.

Business tenants should also provide the payment evidence to their bookkeeping or accounting team.

What Businesses and Self-Employed Persons Should Review

Companies and self-employed persons renting property in Cyprus should perform a broader review of their rental payment and documentation procedures.

Existing Lease Agreements

Check whether the lease requires cash payment, payment in person or another method that may be inconsistent with the new requirements. Where necessary, the parties should document the revised payment procedure in writing.

Standing Orders and Recurring Payments

Where rent is already paid through a standing order, confirm that:

- the recipient account is correct;

- the amount corresponds with the current lease;

- the payment date is appropriate;

- the transaction description is clear; and

- any rent increases have been reflected.

Bookkeeping and Accounting Records

The accounting entry should be supported by the underlying lease, invoice or receipt where applicable, electronic transaction record and relevant correspondence. Businesses using professional bookkeeping services in Cyprus should ensure that the bookkeeping provider receives sufficient evidence to reconcile each rental expense with the corresponding payment. The lease, accounting entry and electronic payment should form one consistent documentary trail.

Related-Party Rental Arrangements

Rent paid to shareholders, directors, connected persons or related entities should be supported by:

- a valid rental agreement;

- identifiable commercial terms;

- electronic payment evidence;

- consistent accounting treatment; and

- appropriate tax reporting.

Electronic payment does not replace the need to demonstrate that the rental expense is genuine, commercially supportable and incurred for business purposes. Businesses that need assistance assessing a related-party lease or the deductibility of rental expenses should obtain appropriate tax planning services in Cyprus before submitting the relevant tax return.

Recommended Supporting Documentation

Landlords, tenants and businesses should retain:

- the signed lease agreement;

- lease amendments or payment notices;

- the landlord’s payment instructions;

- bank transfer confirmations;

- card transaction records;

- electronic payment receipts;

- rental invoices or receipts where relevant;

- correspondence with the landlord or tenant;

- general ledger records; and

- reconciliations between rental records and payments.

The objective is to maintain a complete audit trail from the contractual rental obligation to the actual payment and its accounting treatment. For corporate tenants, rental documentation should form part of the company’s wider financial and compliance records. Appropriate corporate services in Cyprus may also be relevant where the lease is connected with a company’s registered office, operating premises, governance arrangements or substance requirements.

Cyprus Rent Payment: Common Compliance Mistakes to Avoid

Continuing to Pay or Accept Cash

Long-standing practice is not an exemption. Existing cash arrangements should be discontinued before the rules take effect.

Continuing to Apply the €500 Threshold

Earlier articles frequently referred to €500, but the latest official position confirms that the obligation applies regardless of the rent amount.

Using an Unclear Payment Reference

A payment reference should allow the transaction to be connected with the relevant lease, property and rental period.

Paying through an Unrelated Third Party

Payments from an unrelated person or account may create unnecessary questions about who incurred and settled the expense.

Keeping Only a Receipt

A receipt may support the transaction, but it does not replace the required electronic payment record.

Failing to Update the Bookkeeping Team

Accounting personnel should be aware that the payment method may directly affect the tax treatment of the expense.

Assuming Residential Rent Is Excluded

The requirement applies regardless of the type or use of the property. Residential rental arrangements should therefore also be reviewed.

Assuming Small Rent Payments Can Still Be Made in Cash

The latest official clarification does not retain the previously reported €500 threshold. Landlords and tenants should not assume that lower-value rent payments are exempt.

Cyprus Electronic Rent Payment Checklist

Before 1 July 2026, confirm that:

- rent will be paid electronically from the effective date;

- the payment method is accepted under Article 48A;

- cash payment arrangements have been discontinued;

- the tenant has the correct recipient details;

- the lease and payment instructions are aligned;

- each transaction contains a clear reference;

- electronic evidence is retained;

- bookkeeping entries correspond with the payment records;

- staff responsible for payments have been informed;

- related-party rental arrangements are properly documented; and

- earlier internal guidance referring to the €500 threshold has been updated.

How IBCCS TAX Can Assist

The mandatory electronic payment framework affects tax deductibility, bookkeeping, lease administration and wider business compliance. IBCCS TAX can assist companies, self-employed persons, landlords and other taxpayers with:

- reviewing rental payment procedures;

- assessing the tax treatment and deductibility of rental expenses;

- aligning payment records with bookkeeping;

- reviewing supporting documentation;

- identifying gaps in the payment audit trail;

- reviewing related-party rental arrangements;

- updating internal compliance procedures; and

- supporting broader Cyprus tax and accounting compliance.

Our team provides coordinated accounting services in Cyprus, bookkeeping support and tax advisory for local and international businesses operating in Cyprus.

Cyprus Rent payment Rules: Prepare for the 1 July 2026 Effective Date

The new rules establish a clear link between the method of payment, the supporting audit trail and the tax treatment of rental expenditure. Although earlier market commentary frequently referred to a €500 threshold, the latest official clarification confirms that electronic payment is required regardless of the rent amount or property use. Landlords, tenants and businesses should therefore update their payment procedures, leases, bookkeeping instructions and internal guidance before the first rent payment due on or after 1 July 2026.

Contact IBCCS TAX to review the tax, accounting and compliance implications of your rental arrangements in Cyprus.

Frequently Asked Questions

1. When do mandatory electronic rent payments begin in Cyprus?

The requirement takes effect on 1 July 2026.

2. Does the rule apply only to rent of €500 or more?

No. Earlier publications referred to a €500 threshold, but the latest official Cyprus Tax Department announcement confirms that the requirement applies regardless of the rent amount.

3. Which rent payments are covered?

The obligation applies to rent relating to immovable property located in Cyprus.

4. Does the rule apply to residential property?

Yes. The latest official position applies regardless of the type or use of the property.

5. Does the rule apply to commercial property?

Yes. It covers rent for offices, shops, warehouses, industrial premises and other commercial property located in Cyprus.

6. Does it apply to companies and individuals?

Yes. The requirement applies to natural persons and legal entities involved in rental arrangements concerning immovable property in Cyprus.

7. Can rent still be paid in cash?

Cash is not one of the permitted payment methods under Article 48A.

8. Can a landlord accept cash and issue a receipt?

A receipt does not make a cash payment compliant with the electronic payment requirement. The payment itself must be made through an accepted electronic method.

9. Which payment methods are accepted?

Bank transfers, debit or credit card payments and other recognised electronic payment methods are permitted.

10. Can rent be paid through Revolut or another payment platform?

Potentially, provided that the platform constitutes a recognised electronic payment method and creates an adequate, verifiable transaction record. The particular platform and payment arrangement should be assessed where there is uncertainty.

11. What happens if a business pays rent in cash?

The rental expense may not qualify as tax-deductible, potentially increasing the business’s taxable profit.

12. Should existing leases be amended?

Leases should be reviewed where they refer to cash payments or contain unclear or outdated payment instructions. Any revised procedure should be documented in writing.

13. What records should tenants retain?

Tenants should retain the lease, payment instructions, electronic transaction evidence, payment references and relevant correspondence.

14. What records should landlords retain?

Landlords should retain the lease, bank statements, transaction confirmations, rental schedules and records supporting the correct declaration of rental income.

15. Do existing standing orders need to be changed?

Not necessarily. However, the account details, rental amount, payment date and transaction reference should be reviewed to ensure that the standing order corresponds with the current lease.

Cyprus Rent Payment Rules from 1 July 2026: Mandatory Electronic Payments Explained

From 1 July 2026, rent relating to immovable property located

Read More

Cyprus Personal Income Tax Return 2025: IR1 Submission Now Open

The Cyprus Tax Department has announced that the electronic submission

Read More

IBCCS TAX at Global Tech Weekend Tbilisi 2026: Cross-Border Business, Investment and Legal Strategy

IBCCS TAX will take an active role in Global Tech

Read MoreThis publication is provided for general information purposes only.. It does not constitute legal, accounting or tax advice. The application of the rules should be considered in light of the specific facts and any further guidance issued by the Cyprus Tax Department.